The Board of Directors of Axis Bank Limited approved the financial results for the quarter ended 30 th June 2024 at its meeting held in Mumbai on Wednesday, 24th July 2024. This quarter, Axis Bank's focus on collaboration continued to drive innovation. A leader in the acquiring business, Axis Bank partnered with Mastercard to launch NFC Soundbox, an industry-first proposition for the merchant community that enables them to accept various payment methods.

It expanded its omni-channel shopping segment through its Credit Card partnership with Shoppers Stop, offering an enriching online and offline shopping experience. Axis Bank is constantly working to empower the agricultural sector and the farmer community. The Bank signed an MOU with VST Tillers Tractors to offer financial solutions to farmers for purchasing equipment through its extensive branch network.

To boost insurance penetration and financial inclusion, Axis Bank joined forces with Bajaj Allianz General Insurance offering a comprehensive suite of General Insurance products. The Bank continues to advance its commitment towards CSR and Sustainability, Diversity and Inclusion. Axis Bank Foundation launched its first artisan-focused, nation-wide skill-development initiative, aiming to equip over 300 rural artisans.

The Bank was recognised with two titles by the Asia Book of Records for its nationwide cleanliness drive 'Open for the Planet Clean-A-Thon'. It launched 'ARISE ComeAsYouAre', a program that focuses on skill-based hiring, welcoming dynamic LGBTQIA+ individuals into its fold.

Axis Bank garnered a multitude of accolades including ‘The Asian Banker - Global Financial Technology Innovation Awards 2024’ for Best API and Open Banking Implementation and Best Mobile Banking Technology Implementation; ‘Digital CX Awards 2024’ for Best Wholesale Bank for APIs and the ‘Infosys Finacle Innovation Awards 2024’ in 5 categories.

Amitabh Chaudhry, MD&CEO, Axis Bank said, ‘The last quarter was crucial in terms of getting all the teams to work together for the last leg of Citi integration. I am delighted that the integration is done and it was largely seamless given the size and scale of the transition. I am thankful to the teams who worked tirelessly in making this possible, and to our 2 million new customers for keeping their trust and faith in us.’

Amitabh Chaudhry, MD&CEO, Axis Bank said, ‘The last quarter was crucial in terms of getting all the teams to work together for the last leg of Citi integration. I am delighted that the integration is done and it was largely seamless given the size and scale of the transition. I am thankful to the teams who worked tirelessly in making this possible, and to our 2 million new customers for keeping their trust and faith in us.’

Profit & Loss Account: Period ended 30th June 2024

Core Operating Profit and Net Profit

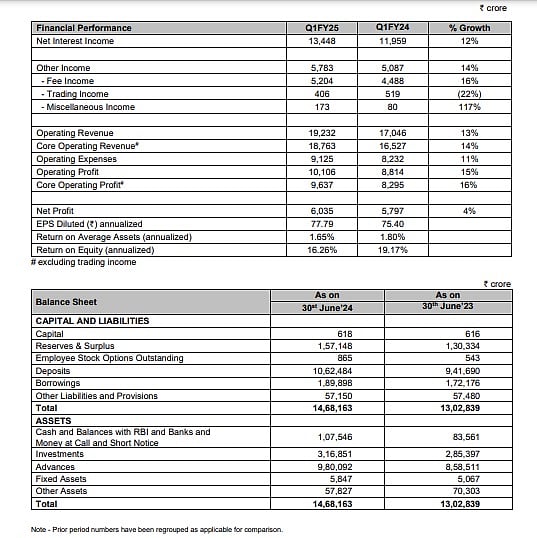

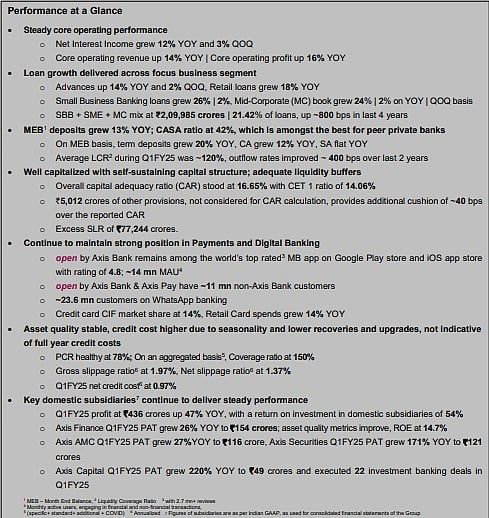

The Bank’s core operating profit for the quarter grew 16% YOY to `9,637 crores. Operating profit grew 15% YOY to `10,106 crores. Net profit stood at `6,035 crores in Q1FY25 as compared to `5,797 crores in Q1FY24, and grew 4% YOY.

Net Interest Income and Net Interest Margin

The Bank’s Net Interest Income (NII) grew 12% YOY and 3% QOQ to `13,448 crores. Net interest margin (NIM) for Q1FY25 stood at 4.05%.

Other Income

Fee income for Q1FY25 grew 16% YOY to `5,204 crores. Retail fees grew 18% YOY; and constituted 71% of the Bank’s total fee income. Retail cards and payments fee grew 12% YOY. Retail Assets (excluding cards and payments) fee grew 13% YOY. Fees from Third Party Products grew 68% YOY. The Corporate & Commercial banking fees together grew 12% YOY and 1% QOQ to `1,497 crores. The trading income gain for the quarter stood at `406 crores; miscellaneous income in Q1FY25 stood at `173 crores. Overall, non-interest income (comprising of fee, trading and miscellaneous income) for Q1FY25 grew 14% YOY to `5,783 crores.

Provisions and contingencies

Provision and contingencies for Q1FY25 stood at `2,039 crores. Specific loan loss provisions for Q1FY25 stood at `2,551 crores. The Bank holds cumulative provisions (standard + additional other than NPA) of `11,732 crores at the end of Q1FY25. It is pertinent to note that this is over and above the NPA provisioning included in our PCR calculations. These cumulative provisions translate to a standard asset coverage of 1.20% as on 30 th June, 2024. On an aggregated basis, our provision coverage ratio (including specific + standard + additional) stands at 150% of GNPA as on 30th June, 2024. Credit cost (annualized) for the quarter ended 30th June, 2024 stood at 0.97%.

Balance Sheet: As on 30 th June 2024

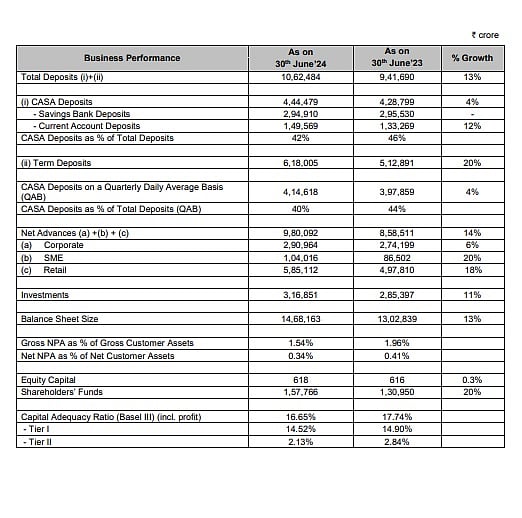

The Bank’s balance sheet grew 13% YOY and stood at `14,68,163 crores as on 30 th June 2024. The total deposits grew 13% YOY on month end basis, of which current account deposits grew 12% YOY; total term deposits grew 20% YOY and 1% QOQ. The share of CASA deposits in total deposits stood at 42%.

On QAB basis, total deposits grew 14% YOY and 3% QOQ, within which savings account deposits grew 3% YOY and 3% QOQ, current account deposits grew 8% YOY and 2% QOQ; and total term deposits grew 21% YOY and 4% QOQ. The Bank’s advances grew 14% YOY and 2% QOQ to `9,80,092 crores as on 30 th June 2024.

Gross of transfers through Inter Bank Participation Certificates (IBPC), total Bank advances grew 15% YOY and 1% QOQ. Retail loans grew 18% YOY to `5,85,112 crores and accounted for 60% of the net advances of the Bank. The share of secured retail loans$ was ~ 71%, with home loans comprising 28% of the retail book. Home loans grew 6% YOY, Personal loans grew 29% YOY, Credit card advances grew 22% YOY, Small Business Banking (SBB) grew 26% YOY and 2% QOQ; and rural loan portfolio grew 24% YOY.

SME book remains well diversified across geographies and sectors, grew 20% YOY to `1,04,016 crores. Corporate loan book (gross of IBPC sold) grew 10% YOY; domestic corporate book grew 7% YOY and 4% QOQ. Mid-corporate book grew 24% YOY and 2% QOQ. 89% of corporate book is now rated A- and above with 89% of incremental sanctions in Q1FY25 being to corporates rated A- and above.

The book value of the Bank’s investments portfolio as on 30 th June 2024, was `3,16,851 crores, of which `2,47,795 crores were in government securities, while `56,384 crores were invested in corporate bonds and `12,672 crores in other securities such as equities, mutual funds, etc. Out of these, 67% are in Held till Maturity (HTM) category, 12% of investments are Available for Sale (AFS), 19% are in Fair Value through Profit & Loss (FVTPL) category and 2% are investments in Subsidiaries and Associate.

Payments and Digital The Bank issued ~1 million new credit cards in Q1FY25 and has been one of the highest credit card issuers in the country over last ten quarters. The Bank continues to remain among the top players in the Retail Digital banking space.

96% - Share of digital transactions in the Bank’s total financial transactions by individual customers in Q1FY25 70% - Individual Retail term deposits (by value) opened digitally in Q1FY25 75% - SA accounts opened through tab banking in Q1FY25 78% - New mutual fund SIPs sourced (by volume) through digital channels in Q1FY25 61% - YOY growth in total UPI transaction value in Q1FY25 50% - YOY growth in mobile banking transaction volumes in Q1FY25 The Bank’s focus remains on reimagining end-to-end journeys and transforming the core and becoming a partner of choice for ecosystems.

Axis Mobile is among the world’s highest rated mobile banking app on Google Play store and iOS app store with rating of 4.8 and over 2.7 million reviews. The Bank’s mobile app continues to see strong growth, with Monthly Active Users of ~14 million and nearly ~11 million non-Axis Bank customers using Axis Mobile and Axis Pay apps.

The Bank has been among the first to go live on Account Aggregator (AA) network and has seen strong initial traction in AA based digital lending. The Bank has 410+ APIs hosted on its API Developer Portal.

On WhatsApp banking, the Bank now has over ~23.6 million customers on board since its launch in 2021. Wealth Management Business – Burgundy The Bank’s wealth management business is among the largest in India with assets under management (AUM) of `5,99,108 crores as at end of 30 th June 2024 that grew 40% YOY and 12% QOQ. Burgundy Private, the Bank’s proposition for high and ultra-high net worth clients, covers 13,071 families. The AUM for Burgundy Private increased 31% YOY and 14% QOQ to `2,09,451 crores.

Capital Adequacy and Shareholders’ Funds

The shareholders’ funds of the Bank grew 20% YOY and stood at `1,57,766 crores as on 30 th June 2024. The Bank now has a self-sustaining capital structure to fund growth, with organic net capital accretion through profits to CET-1 of 32 bps for the Q1FY25. As on 30th June 2024, the Capital Adequacy Ratio (CAR) and CET1 ratio was 16.65% and 14.06% respectively. Additionally, `5,012 crores of other provisions, is not considered for CAR calculation, providing cushion of ~40 bps over the reported CAR. The Book value per equity share increased from `425 as of 30 th June, 2023 to `511 as of 30th June, 2024.

Asset Quality

As on 30 th June, 2024 the Bank’s reported Gross NPA and Net NPA levels were 1.54% and 0.34% respectively as against 1.43% and 0.31% as on 31st March, 2024. Recoveries from written off accounts for the quarter was `591 crores. Reported net slippages in the quarter adjusted for recoveries from written off pool was `2,700 crores, of which retail was `2,456 crores, CBG was `13 crores and Wholesale was `231 crores. Gross slippages during the quarter were `4,793 crores, compared to `3,471 crores in Q4FY24 and `3,990 crores in Q1FY24. Recoveries and upgrades from NPAs during the quarter were `1,503 crores. The Bank in the quarter wrote off NPAs aggregating `2,206 crores. As on 30 th June, 2024, the Bank’s provision coverage, as a proportion of Gross NPAs stood at 78%, as compared to 80% as at 30th June, 2023 and 79% as at 31st March, 2024. The fund based outstanding of standard restructured loans implemented under resolution framework for COVID-19 related stress (Covid 1.0 and Covid 2.0) declined during the quarter and as at 30 th June, 2024 stood at `1,409 crores that translates to 0.13% of the gross customer assets. The Bank carries a provision of ~ 20% on restructured loans, which is in excess of regulatory limits.

Network

The Bank added 50 branches during the quarter, taking its overall distribution network to 5,427 domestic branches and extension counters along with 182 BCBO’s situated across 2,987 centres as at 30th June, 2024 compared to 4,945 domestic branches and extension counters, and 156 BCBO’s situated in 2,754 centres as at 30 th June, 2023.

As on 30th June, 2024, the Bank had 15,014 ATMs and cash recyclers spread across the country. The Bank’s Axis Virtual Centre is present across six centres with over ~1,600 Virtual Relationship Managers as on 30 th June 2024.

Key Subsidiaries’ Performance

The Bank’s domestic subsidiaries delivered steady performance with Q1FY25 PAT of `436 crores, up 47% YOY.

Axis Finance: Axis Finance has been investing in building a strong customer focused franchise. Its overall assets under finance grew 37% YOY. Retail book grew 51% YOY and constituted 46% of total loans. The focus in its wholesale business continues to be on well rated companies and cash flow backed transactions. Axis Finance remains well capitalized with total Capital Adequacy Ratio of 19.35%.

The book quality remains strong with net NPA at 0.29%. Axis Finance Q1FY25 PAT was `154 crores, up 26% YOY from `123 crores in Q1FY24. Axis AMC: Axis AMC’s overall QAAUM grew 18% YOY to `2,91,967 crores. Its Q1FY25 PAT was `116 crores, up 27% YOY from `91 crores in Q1FY24.

Axis Capital: Axis Capital Q1FY25 PAT was `49 crores, up 220% YOY from `15 crores in Q1FY24 and completed 22 investment banking transactions in Q1FY25.

Axis Securities: Axis Securities’ revenues for Q1FY25 grew 118% YOY to `426 crores. Its Q1FY25 PAT grew 171% YOY and stood at `121 crores.