Viral Acharya, a C.V. Starr Professor of Economics in the Department of Finance at New York University Stern School of Business (NYU-Stern) and former deputy governor of Reserve Bank of India (RBI), delivered the keynote address for the five-part webinar series on the Future of Banking. The session focused on Embedded Finance and MSMEs accompanied by the right technology which will change the way lending will take place in the future.

Acharya, an Academic Advisor to the Federal Reserve Banks of New York and Philadelphia, has also written about this in his book ‘Quest for Restoring Financial Stability in India’

The session was moderated by FPJ, consulting editor, RN Bhaskar.

Today, look at the landscape of banking in India and at the progress India has made in technology. Banking cannot remain untouched by the technological revolution in India, while other sectors explore it.

The Future of Banking in India will depend on the way India will embrace technology going forward — still pursuing their traditional function of extending credit for those who can put it for productive use in the economy.

The credit landscape is full of paradoxes. On one hand, Indian banks have the highest non-performing asset ratio (NPAs) in the world, on the other, India does not have a lot of credit penetration in terms of credit to GDP. Normally, NPAs are high among countries which are usually overbanked. But for segments of India, especially micro, small and medium-sized enterprises, it is not true.

Banks, who are in the business of providing formal credit, only cater to 16 per cent of the demand. Most of the MSMEs credits are actually informal. Therefore, it is outside of the banking system. Typically, within the MSMEs, the banking credit is generally extended to those firms with higher turnover.

Reports like RBI’s UK Sinha MSME report 2019 and IFC Financing MSME report of 2018, have noted that the situation of formal credit to MSMEs in India is more like a tip of an iceberg. There is a lot of demand that is not visible. It is informal. It tends to be small loans at a high-interest rate. It does not tend to have a customised nature that MSMEs typically need. MSMEs have had a rough landing in the economy for one reason or the other over the last five years.

In any part of the world, including developed countries like the United States (US), MSMEs are the largest employers. Meanwhile, in India, MSMEs have not thrived as per their potential. There are many reasons for this. But one wonders if the lack of access to formal credit is one such reason.

The informal finance of India right now is arranged in a very complex manner. Here no one knows who is connected to whom. There is a set of potential financiers and borrowers. There are attempts made to reduce lender and borrower distances by appointing various kinds of agents and in that process all kinds of complex linkages are being set up. However, in the end, the level of credit extension that we create for formal finance is not that large.

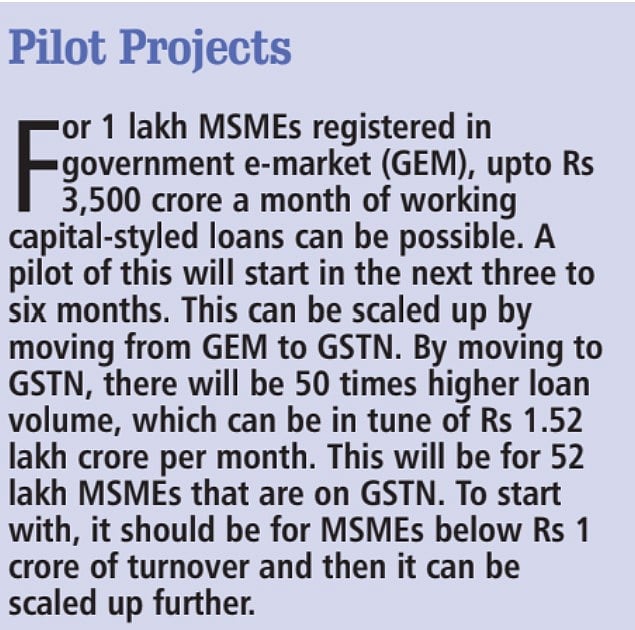

Right at the centre, there are banks. Right at the upper rim, there are MSMEs. MSMEs are interacting with different platforms for different aspects like dealing with GSTN, GEM, online platforms and other intermediaries — these are the entities in the intermediaries rim. They are connected to MSMEs on the outside. This will allow banks to travel to the MSMEs with help of these intermediaries very quickly.

Not under one institution, says Viral Acharya

I am not a big fan of concentrating everything into a single entity. I like the idea of banks doing finance and doing the job of taking deposits and extending credits. We generally do not like the heavy-handed regulations of industrial companies or non-financial companies. I think embedded finance is a middle ground. In a structure of an economy, you will get a resilient system if different entities perform their task well and systems are differentiated functionally. I am not proposing that these LSPs become credit extension agencies -- that could be a mistake. We cannot mix finance with commerce. We will run into problems. The way banks became too systemic to fail and then industries will become too big to fail as well. This would mean all risks will be socialised and there will be no risks left to be borne by private players.

Next generation credit model

Indian banks will have to fill this gap in the future. To do that, banks need to embrace the next generation MSME credit model called ‘Embedded Finance’ in three shifts:

-Agent of the borrower;

-Values information collateral; and

-Structured high-trust data ecosystem

What is embedded finance?

Traditional finance provided to MSMEs is asset-based lending. It looks for physical collateral and is a heavily paper-based process. Loan for MSMEs is a very traditional loan approval system. There is a lot of documentation work even though it has been digitised. Even the agents/officers, whom banks deploy for banking services, usually do not exist in the MSME’s ecosystem.

Banks and MSMEs are distant from each other. Even the intermediaries that are getting deployed are not in proximity to the MSME in terms of business transactions and other activities.

There are several problems that this creates. Many small and micro enterprises may not have physical collateral. So, you cannot do asset-based lending. Such MSMEs are generally providing services around the areas where they are located. Ideal loans to them are not necessarily of very large quantum but about maturity profile and cash flow that is tied to the working capital profile of the MSMEs. To know the levels of this cash flow pattern of MSMEs, it would be ideal that banks appoint loan service providers (LSP) as intermediaries.

Embedded finance is essentially that lenders should not get close to MSMEs by appointing agents that have nothing to do with MSMEs. The banks should instead work with LSPs who already have tentacles into the MSME ecosystem because they are providing value-based services.

Agent of the borrower/ loan service provider (LSP)

LSP could be anyone like a kirana tech, agri-tech, legal tax filing app, GSTN (Goods and Services Tax Network) or government e-marketplace, Swiggy, Amazon, Flipkart, Big Bazaar anyone evolved in the supply chain of the MSME. These are agents who are in proximity to the MSME ecosystem. Banks should engage with these natural partners.

Value information collateral

Many MSMEs, especially services-based MSMEs, do not have physical collateral. So, their collateral should be information about their cash flow, transactions, financing of MSMEs among other information. A public credit registry which can potentially contain all the information regarding the liabilities will be needed.

There is a need to keep a central (transaction) registry. Of course, account aggregators and public registry are in principle the data sources for providing the financial balance sheet history. But the transaction registry will have to be with LSPs. This is mainly because LSPs are embedded in the ecosystem of the MSMEs. This will enable the shift from asset-based lending to information-based lending.

Historically, LSPs have tried to perform the function. But because of the bureaucratic paper-based system and physical collateral intensive credit system, these arrangements were never successful.

Structured high-trust data ecosystem

Rather than keeping the MSMEs informal and then being in a system that is data poor, the financial ecosystem/ the bank credit system can evolve to a system wherein MSMEs would find it worthwhile to formalise and to provide data to account aggregators and public credit registry.

The data along with transaction registry with the LSPs can be provided with consent and adequate privacy safeguards to the banks. By using the data, the banks can assess the type of loans they want to issue, the quantum of the loan and its maturity. It would be possible in the system that is data rich, rather than data poor.

Open Credit Enablement Network (OCEN)

It is essentially part of the IndiaStack. It is part of the APIs which provide a common set of applications or utilities. There LSPs or intermediaries are able to access information freely even though they have access to some information. Several lenders can access the information. OCEN is a set of open APIs that enables the competition. More than 90 customer-facing entities are engaging to become OCEN-enabled LSPs like tax and legal filing applications, neobanks, accounting & khata app companies, kirana tech, supply chain financiers, B2B e-commerce, social networks, agri-tech, payment gateways, and loan selection platforms.

Benefits of Embedded Finance

The benefit of embedded finance is that we can visualise the architecture of the future of bank extension of credit to MSMEs. This is possible in the following way:

Banks that enjoy low-cost capital will now approach a set of intermediaries that are part of the MSME ecosystem and hire them as potential LSPs.

Banks should engage with institutions that are connected with MSMEs for business. Reputational linkage has a tremendous advantage.

Digitalisation of borrower information will bring down cost. The borrower just has to give consent to the lender; and the lender will just need to process the data either with artificial intelligence or machine learning or some human intervention. So, the loan is provided to the borrower through the LSP quickly. In this, technology is the key.

To make embedded finance a success, what steps need to be taken:

Reduce the transaction cost which is possible only if all talk in common language: Information collateral has to substitute physical collateral. That information collateral will have to travel seamless back and forth. It is about the transaction and financial balance sheet of the MSMEs.

Enforce payment: Once credit is originated, you have to ensure that you do not appoint a recovery agent to recover money. But ensure that the system (read intermediaries) will entrap the repayment that has to be made to the bank.