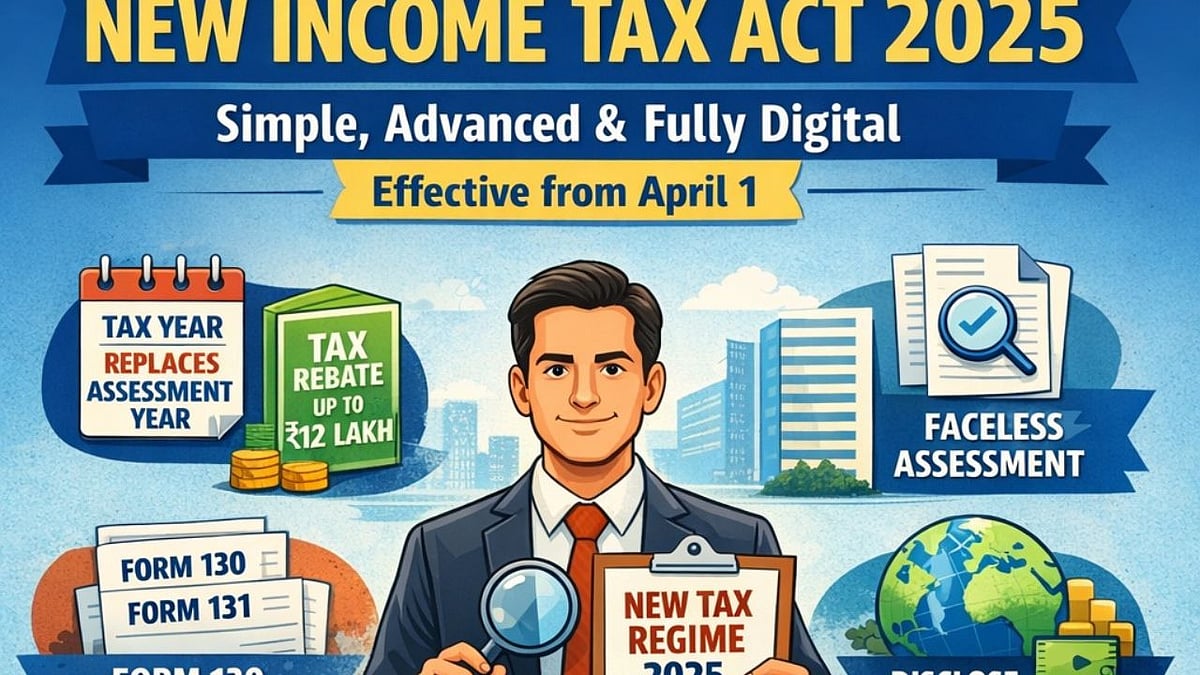

New Delhi: From April 1, India has introduced the Income Tax Act 2025, replacing the six-decade-old Income Tax Act of 1961. The new law aims to simplify the tax system, make rules easier to understand, and reduce legal disputes.

The government has used simpler language and removed outdated provisions to improve compliance among taxpayers.

Introduction of ‘tax year’ concept

One of the biggest changes is the introduction of the 'tax year.' This replaces the earlier system of financial year and assessment year, making tax filing easier to understand.

However, there are no changes in the existing tax slabs under the old or new regimes.

New return filing deadlines

The new law changes the deadlines for filing income tax returns based on different categories of taxpayers.

Individuals filing simple returns will have time till July 31. Those with business or professional income without audit requirements can file till August 31. Companies and audited cases will have time till October 31, while special cases can file till November 30.

These timelines will apply from the tax year 2026–27.

More time for revised returns

Taxpayers now get more time to correct mistakes. The deadline for filing revised returns has been extended from 9 months to 12 months.

However, a fee will be charged if returns are filed after 9 months. The penalty is Rs 1,000 for income up to Rs 5 lakh and Rs 5,000 for higher income.

Changes in taxes and transactions

The government has increased Securities Transaction Tax (STT) on certain derivative trades. At the same time, Tax Collected at Source (TCS) on education and medical remittances abroad above Rs 10 lakh has been reduced from 5 percent to 2 percent.

Buyback income will now be taxed as capital gains. Also, tax benefits on Sovereign Gold Bonds will be limited only to those bought at the original issue price.

Other key changes

Interest earned on motor accident compensation will now be tax-free. Travel expenses provided by employers for commuting from home to office will not be treated as taxable benefits.

The process of TDS on property purchases from non-residents has also been simplified by allowing PAN-based payments.