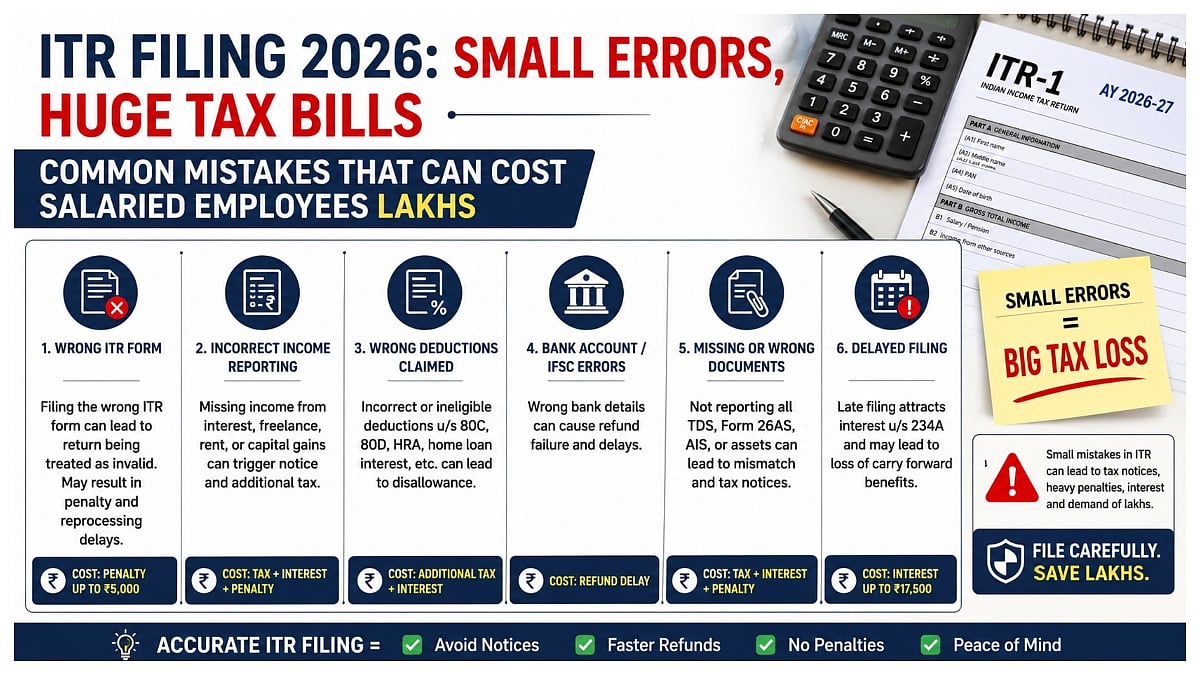

Mumbai: Filing an Income Tax Return (ITR) is no longer as simple as copying figures from Form 16. With the Income Tax Department using data from Form 26AS, the Annual Information Statement (AIS) and the Taxpayer Information Summary (TIS), even small mistakes can lead to tax notices, extra tax, interest and penalties.

Employees should reconcile salary details with bank statements, investment records, capital gains statements and other financial documents before filing.

Income from bank interest, fixed deposits, dividends, rental property or freelance work must also be reported if applicable.

Choose Tax Regime Carefully

Many salaried taxpayers select the old or new tax regime without comparing the total tax liability under both options.

The new regime offers lower tax rates but limits many exemptions and deductions, including HRA, LTA, home loan interest and several deductions under Sections 80C and 80D.

Employees should calculate tax under both regimes before making a choice. Those with business income should also remember that switching rules are more restrictive.

Claim Deductions Correctly

Claiming deductions without valid proof is another common mistake. Taxpayers sometimes declare investments to their employer but fail to make them before the financial year ends.

Before claiming deductions, verify insurance premiums, ELSS investments, provident fund contributions, home loan certificates and donation receipts to avoid future tax demands.

Report All Income

Capital gains from shares, mutual funds, ESOPs or property must be reported correctly. Errors in calculating long-term or short-term gains, acquisition cost or exemptions can result in higher tax liability.

Bonus, arrears, joining bonus, severance pay and retirement benefits also require proper tax treatment. Some payments may qualify for relief under Section 89, while others are fully taxable.

Foreign Assets And Refund Checks

Resident and ordinarily resident taxpayers must disclose foreign assets, overseas bank accounts, ESOPs and foreign income wherever applicable. Failure to do so may attract heavy penalties under the Black Money Act.

Before filing, ensure bank account details are correct, linked with PAN and pre-validated to avoid refund delays.

Finally, e-verify the ITR within the prescribed timeline. An unverified return may be treated as invalid, delaying refunds and inviting further compliance issues.

Careful reconciliation, proper documentation and timely verification can help employees avoid costly mistakes while ensuring all eligible tax benefits are claimed.