Mumbai: “If a bitter seed (karaskaram) is soaked in milk for years, will its bitterness disappear?”

The ancient proverb remains uncomfortable because it asks a question that every generation believes it has already answered. Yet history continues to disagree.

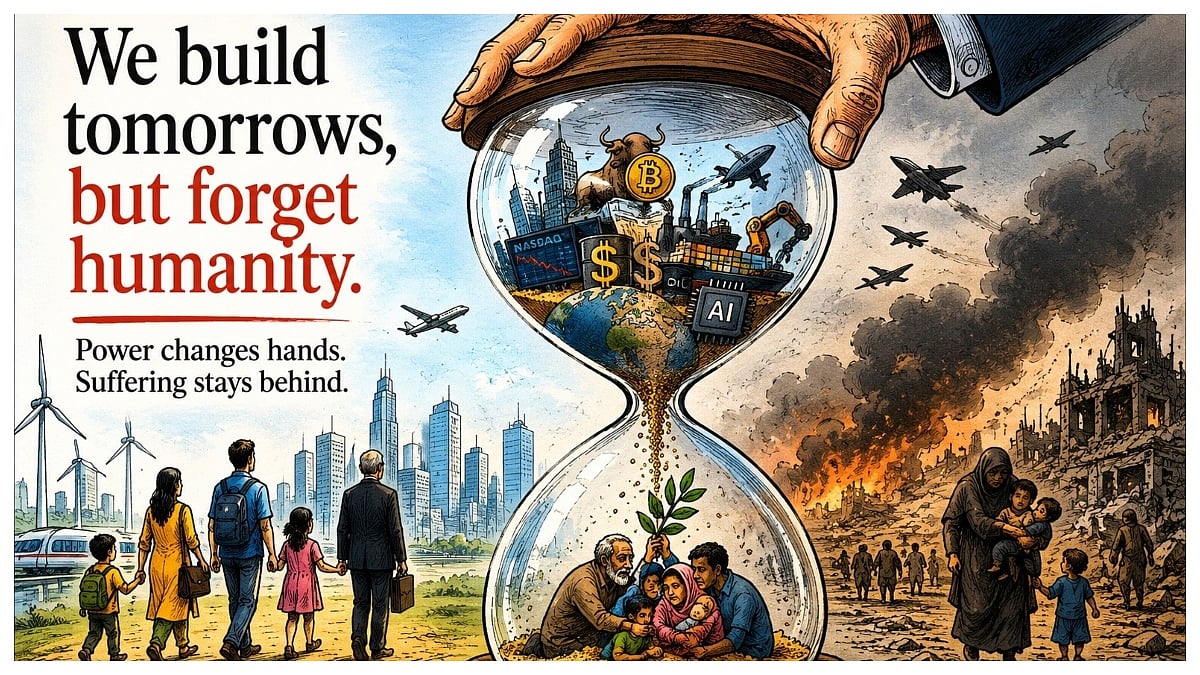

The first week of June offered another reminder that prosperity does not necessarily civilise humanity. Wealth grows. Technology advances. Nations become richer. Cities become taller. Artificial intelligence becomes smarter. Yet the oldest weaknesses of civilisation continue to survive beneath the surface.

From New Delhi to Washington, from Moscow to Tel Aviv, from Tehran to Beijing, from Brussels to London, and from Africa to Australia, the world remains trapped between extraordinary progress and familiar conflict. Economies expand, technologies evolve and markets innovate, yet many of humanity's oldest disputes continue to shape the modern age.

The names change. The patterns rarely do.

From Jawaharlal Nehru to Indira Gandhi, from Atal Bihari Vajpayee to Manmohan Singh and Narendra Modi, from George W. Bush to Barack Obama and Donald Trump, from Tony Blair to Boris Johnson and Keir Starmer, from Mikhail Gorbachev to Vladimir Putin, leaders have come and gone. Yet Iraq gave way to Libya, Libya to Yemen, Yemen to Syria, and the long and painful story of Israel and Palestine continues to cast its shadow across generations. Gaza burns, Lebanon trembles, Iran and Israel confront one another, and fresh uncertainties spread across West Asia. Entire generations of children have grown up knowing conflict more intimately than peace, while countless families have buried dreams that never had the opportunity to mature.

The economic consequences are never far behind.

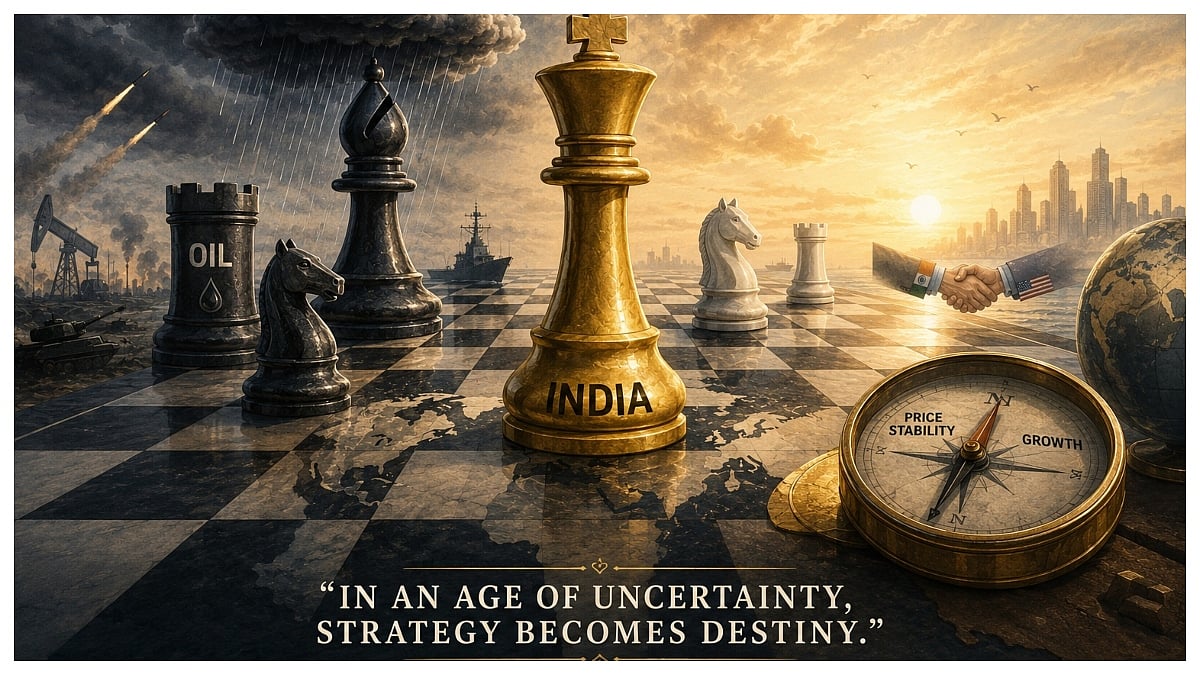

This week, the Reserve Bank of India kept interest rates unchanged while lowering growth forecasts and raising inflation projections. Governor Sanjay Malhotra's decision reflected a reality that every central banker understands: markets may trade on numbers, but economies often move on human behaviour.

Oil remains the world's most powerful messenger. A missile launched in one region can alter transport costs, food prices, airline fares and household budgets thousands of kilometres away. The Strait of Hormuz, Russia's energy exports, and the policies of Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman and Bahrain continue influencing inflation as surely as any domestic policy.

Trade negotiations between India, the United States, Europe and the United Kingdom seek to build bridges. Yet even as nations speak of partnership, protectionist instincts continue resurfacing. This week, President Donald Trump launched a fresh wave of trade actions after America's top court challenged earlier tariff measures. Washington proposed duties of between 10 and 12.5 per cent on imports from more than sixty countries, including India and the European Union, while also targeting Brazil and examining trade practices in Vietnam and China. The message was familiar: globalisation may be celebrated in speeches, but economic nationalism remains deeply rooted in policy.

Even technology reflects the contradiction. The race for artificial intelligence promises remarkable gains, yet increasingly resembles a contest for dominance rather than collective advancement. American and Chinese technology giants compete fiercely for data, computing power and influence, while concerns grow over imitation, digital monopolies and the future of employment itself.

China's manufacturing strength, America's economic resilience, Europe's inflation concerns, Japan's policy adjustments, Russia's strategic calculations and the Gulf's energy diplomacy all point towards one reality: economics and geopolitics are no longer separate conversations.

The lesson is neither cynical nor pessimistic.

It is simply that economics cannot be separated from human nature.

History repeats itself not because humanity lacks knowledge, but because it often struggles to apply wisdom.

The bitter seed may wear new leaves. It may grow taller branches. It may even produce richer fruit.

Yet unless nations learn to value cooperation as much as competition, and humanity as much as power, the roots beneath the tree will remain remarkably unchanged.

THE WEEK IN HARD NUMBERS

(JUNE 1–7)

Economics often speaks most clearly through numbers.

1. India's economy expanded 7.7% in FY26, while the March quarter grew 7.8%, reaffirming the country's position among the world's fastest-growing major economies. Yet the RBI kept the repo rate unchanged at 5.25%, lowered FY27 GDP growth forecast to 6.6%, and raised its inflation projection to 5.1%, reflecting caution amid rising global uncertainty.

2. Oil remained the week's most influential commodity. Brent crude traded largely between $93 and $95 a barrel, while analysts warned that any serious disruption to the Strait of Hormuz could affect 4–5 million barrels of daily supply, with consequences for inflation, shipping and growth worldwide.

3. Global markets flashed warning signals. The Nasdaq plunged 4.2% on Friday, losing a record 1,121 points and helping erase roughly $1.8 trillion in S&P 500 market value. Japan's Nikkei 225 fell 1.31% to around 66,588 as technology shares weakened.

4. Bitcoin slipped below $60,000 and remains down roughly 33% so far in 2026. More than $3.1 billion has reportedly flowed out of Bitcoin exchange-traded funds this year as investors redirected capital towards artificial-intelligence opportunities.

5. Beyond economics, the human cost of conflict remained immense. Continued instability from Gaza, Lebanon, Iran and the wider West Asian region kept energy, trade and financial markets on edge.

6. On Friday, Europe's biggest telecom deal of the year saw Bouygues, Orange and Iliad agree to acquire SFR for $23.4 billion.

7. Fresh Iranian attacks on Kuwait, Bahrain and the Strait of Hormuz reminded markets that peace in the Gulf remains fragile.

8. FPIs withdrew nearly ₹43K crore from Indian equities in early June, taking 2026 outflows to ₹2.67L crore.

9. Government and RBI measures may boost forex inflows, stabilise the rupee and potentially reverse FPI outflows if the AI-driven investment trend cools.

10. The rupee closed at 94.94 per US dollar on June 5, recovering sharply after RBI and government forex-support measures. The rupee recorded its biggest one-day gain in two months, rising 0.9% following RBI's liquidity and forex initiatives.

11. Market estimates suggest recent RBI and government measures could attract $40–60 billion in foreign capital inflows.

12. RBI announced liquidity-enhancing measures worth around ₹1 lakh crore to strengthen forex reserves and support market stability.

The week's lesson was simple: numbers may appear cold, but behind every statistic stand households, businesses, livelihoods, nations and human lives.