Metal credit cards are no longer a rarity in India. They have become a defined segment in premium banking, with several banks offering cards that combine physical aesthetics with a substantial benefits package.

Cardholders are drawn not just to the physical appeal of the card, but to the suite of benefits that accompany it. The real question is whether these benefits justify the cost.

What sets metal credit cards apart?

A metal credit card differs from a standard PVC card in both construction and positioning.

Key differences include:

· Metal construction that offers a distinct look, feel, and durability compared to traditional PVC cards.

· They offer access to premium lifestyle and travel privileges, such as airport lounge access, concierge services, and exclusive experiences.

· Premium onboarding and customer service experiences tailored to affluent cardholders.

· Accelerated reward structures that can help users earn greater value on their spending.

· Higher annual fees that reflect the premium benefits package and overall card proposition.

The fee structure alone signals the intended audience: individuals with high discretionary spending who can offset the cost through active usage of benefits.

Concierge services

Concierge is among the most marketed features on premium credit cards. In practice, it functions as a dedicated assistance line for tasks such as restaurant reservations, travel bookings, event ticketing, and gift sourcing.

The use of concierge services depends entirely on how frequently a cardholder engages with them. For frequent travellers , a responsive concierge can genuinely save time. For occasional users, it may remain largely untouched.

Points to consider when evaluating concierge value:

· Response time and availability (24/7 vs limited hours).

· Scope of services covered domestically and internationally.

· Quality of recommendations and vendor relationships.

· Whether the service operates in-house or through a third party.

A credit card offering concierge services should be assessed on actual responsiveness, not merely on its presence as a listed feature.

Golf benefits

Golf privileges are a consistent offering on metal and super-premium cards in India. These mostly include complimentary rounds at partner golf courses, access to lessons, and sometimes guest passes.

For cardholders who play golf regularly, the benefit can offset a meaningful portion of the annual fee. A single round at a premium course can cost between ₹2,000 and ₹8,000, making even four to six complimentary rounds per year financially significant.

For non-golfers, however, this benefit holds no realisable value. It is worth identifying whether a card's fee is being partially justified by benefits that do not align with one's lifestyle.

Luxury travel and lounge access

Airport lounge access is one of the most widely used benefits across premium cards. Many metal cards offer enhanced domestic and international lounge access, although the number of complimentary visits and eligibility criteria vary by issuer.

Beyond lounges, luxury travel benefits may include:

· Complimentary hotel night stays or room upgrades at partner properties.

· Priority check-in and baggage handling at select airlines.

· Travel insurance covering lost baggage, trip cancellation and medical emergencies abroad.

· Foreign currency markup waivers or reduced charges.

IDFC FIRST Bank, for instance, positions its Mayura metal credit card within a broader framework that combines travel privileges with lifestyle benefits, targeting cardholders who spend across both categories consistently. The card rewards frequent flyers by pairing zero forex markup and high travel points with four complimentary domestic airport lounge visits each quarter upon hitting a standard monthly spending milestone.

Travel benefits are best evaluated against actual travel frequency. A cardholder who flies domestically four or more times a year and internationally once or twice stands to recover a substantial portion of the annual fee through lounge access and insurance coverage alone.

Reward structures

Premium cards tend to offer accelerated reward rates on categories such as dining, travel, and international spends. Some also offer milestone bonuses upon reaching defined annual spend thresholds.

What distinguishes a well-structured metal credit card reward program:

· Higher earning rates on relevant categories.

· Milestone bonuses that are achievable within realistic spend patterns.

· Flexible redemption options, including statement credit, travel, and merchandise.

· Low or no reward expiry.

Reward value must be calculated against actual redemption, not just earn rates. A high earn rate with limited or poor redemption options reduces net benefit.

Is the annual fee justified?

The simplest framework for assessing value is to list all benefits offered, assign a realistic monetary value to those you would use, and compare the total against the annual fee.

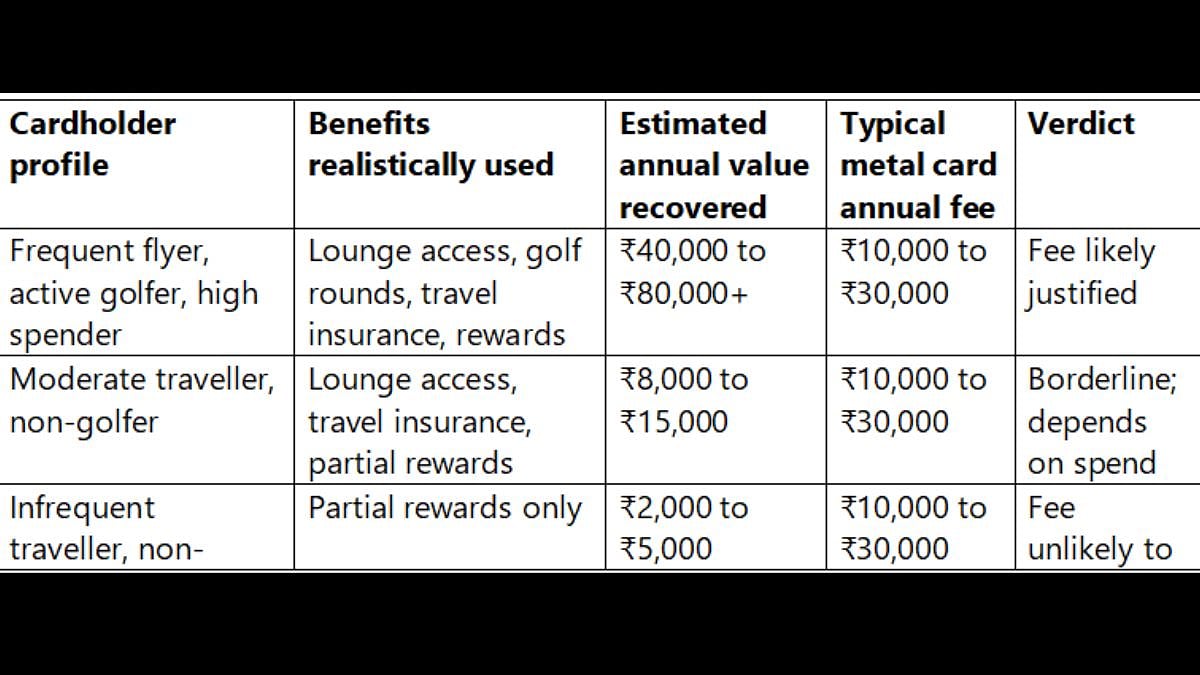

Cardholder profile

Benefits realistically used

Estimated annual value recovered

Typical metal card annual fee

This quickly tells you whether the card is suitable for your lifestyle preferences.

Conclusion

Metal credit cards deliver real value only when their benefits match how you actually live and spend. Concierge, golf, and travel perks are compelling on paper, but their worth is dictated entirely by usage. The simplest test is to map a card's offerings against one's genuine spending habits before committing to the annual fee.