Buying a home loan involves major decision-making. It entails evaluating available options in the market and determining your financial compatibility with them. Understanding how different products compare based on competitive rates, loan tenures, and processing mechanisms is key to choosing the best home loan bank. It means home ownership without burning a hole in your pocket.

Through this blog, we help you conclude. It features criteria you ought to base your home loan comparison on, delves into the numbers, and details the steps you need to take.

Factors to Compare Home Loan Offers On

Every bank proposes unique conditions for home loans based on a few common criteria. Consider the following:

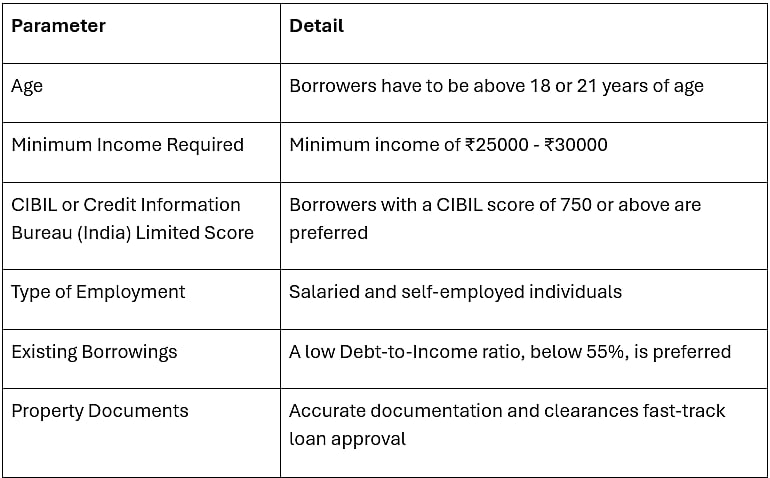

Home Loan Eligibility

You may or may not be eligible for a certain loan amount based on the best home loan bank you choose. Lending institutions typically set these parameters for borrowers:

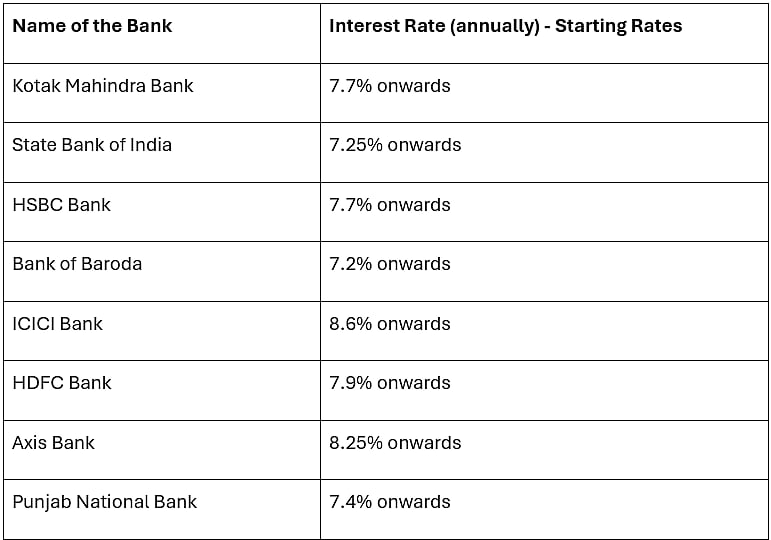

Home Loan Interest Rates 2026

Assessing interest rates provided by different banks helps determine your cost of borrowing and choose the most affordable option. Here are the lender-published interest rates of top lending institutions in 2026:

Note: Interest rate values may vary based on other eligibility criteria.

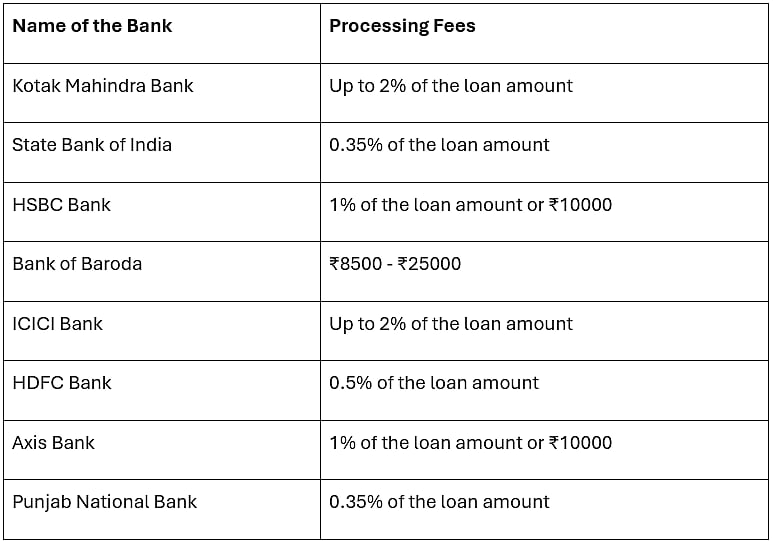

Processing Fees & Additional Charges

Processing your home loan involves expenses on the lender’s part. These include closing costs for different purposes, such as:

● Loan initiation

● Loan appraisal

● Title pursuit

● Insurance, such as PMI (Private Mortgage Insurance)

● Loan discount points

● Recording charges, and more.

While certain institutions charge this amount as a percentage of your loan amount, others charge it on a fixed-term basis. Compare the current processing fees across the best home loan banks to reduce your overall cost of borrowing:

Home Loan Tenure

The tenure specified in a home loan offer determines your EMI and the annual interest you’re liable to pay. It indicates the duration within which you’ll be repaying the complete loan amount.

● Long Tenures

Lengthy home loan tenures come with low EMIs. The principal amount is more widely spread out over a longer period and thus attracts higher interest rates.

● Short Tenures

A short loan tenure means you repay your home loan over a limited period of time. These feature high EMI amounts and low interest rates.

The best home loan banks balance tenure and interest rates to provide a beneficial deal to borrowers.

Ease of Onboarding

Look for the best home loan banks with minimal documentation demands, digital-first loan journeys, quick verification, and doorstep services. The ease of onboarding impacts the speed at which your home can be bought in a competitive market, reduces financial discomfort, and ensures post-purchase formalities are friction-free.

Documents Required to Apply for a Home Loan

Compile these documents in one place, pre-application for a home loan.

● Identity and age proof (Passport, Aadhaar card, PAN, Birth certificate)

● A photocopy of the passbook or bank statements

● Income proof, including Form 16 of the latest assessment year

● Proof of the existence of a business or partnership (for self-employed individuals)

● Proof of repayment track record (wherever applicable)

● All valid property documents and any other information asked for by the lending institution

You can opt for an Home Loan EMI calculator to assess and compare the potential EMI amount you’ll be required to pay based on the conditions proposed by different lenders.

Final Thoughts

Home loans come in various types. Some are for ready-to-move-in properties, while others are for under-construction and plot purchasing decisions. India’s intensely competitive real estate market requires homeowners to plan their home ownership ahead of time.

Instead of directing your savings into a mortgage, based on macro factors you have no control over, the best home loan bank empowers you to manage your finances better in the long term. With a little research and due diligence, you’re able to favourably commit a part of your annual income into your dream home.

FAQs

● Which bank is giving the lowest home loan rate?

Opt for a bank-independent EMI calculator to calculate the interest rate you’ll need to pay on your home loan. Factors such as your credit score, salary, repayment record, and loan-to-value ratio are considered.

● What is the 20-30-40 rule for home loans?

In the case of home loan payments, 20% refers to the down payment you should make. 30% is the limit on the EMI amount proportionate to your annual income, and 40% sets the limit for the total financial expenses flowing out of your income, for the loan.

● How to repay a 25-year home loan in 10 years?

If you’re looking to fast-track loan repayment, increase the monthly EMI amount you’re liable to pay your lender. You can calculate this with an EMI calculator.