A Unit Linked Insurance Plan (ULIP) is a financial product that combines life insurance coverage with market-linked investment opportunities. As living costs grow and individuals live longer lives in retirement, more working Indians are starting on this path earlier than ever before. While traditional choices like provident funds and pension schemes are still significant, ULIP plans are gradually becoming a part of many retirement portfolios. It provides a means of achieving long-term financial objectives while ensuring security by combining life insurance with market-linked assets.

Why retirement planning requires a long-term approach

The topic of returns is frequently brought up while discussing retirement planning. A person who begins investing at age thirty has an edge over a person who waits until age forty-five. The difference is not always about investing larger amounts. More often, it is about giving investments enough time to grow. Compounding works slowly in the beginning, but over long periods, its impact can become substantial.

Inflation is another reason retirement planning cannot be treated as a short-term goal. Expenses that seem manageable today may look very different twenty years from now. Medical costs are a good example.

Spending two decades or more without a monthly pay cheque is becoming more typical. This truth makes steady long-term investing significantly more crucial than one-time gifts.

Understanding how a ULIP Plan works

A ULIP Plan is a single policy that combines market-linked investments with life insurance. A portion of the money paid in premiums is used to provide life insurance coverage. The remaining portion is invested in funds chosen by the policyholder. Depending on individual preferences and financial objectives, these investments may be directed towards equity funds, debt funds, or a combination of both.

The value of the investment component changes according to market performance. Meanwhile, the insurance cover remains available throughout the policy term. For individuals looking to balance protection and long-term wealth creation, this structure offers a practical approach.

How a ULIP Plan supports retirement planning

Several characteristics of a ULIP Plan align naturally with retirement-focused investing.

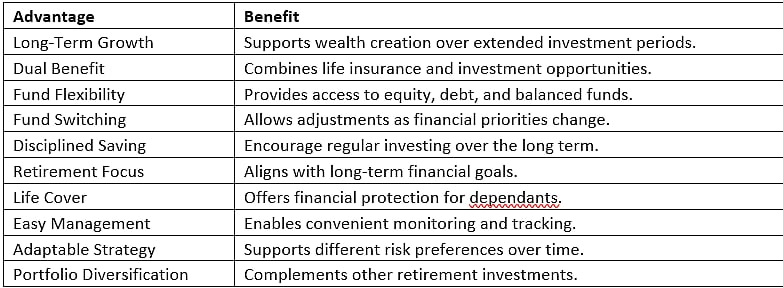

Long investment horizon

Most retirement goals are decades away from the day an investor starts planning. While short-term fluctuations are unavoidable, longer holding periods provide more opportunities for investments to recover volatility and benefit market growth over time.

Flexibility in fund allocation

Few people's financial priorities remain unchanged throughout their careers. A younger professional may be comfortable allocating a larger share towards equity-oriented funds. Many ULIPs allow policyholders to switch between available funds, helping them adjust their investment approach as circumstances change.

Encourages disciplined investing

One aspect that deserves more attention is consistency. Retirement planning is rarely successful because of a single investment decision. It is more frequently the outcome of consistent contributions over a long period of time. Scheduled premium payments support that practice and assist investors in maintaining their long-term goals.

Insurance protection during earning years

Building a retirement corpus is important but protecting family members during the earning phase matters just as much. A ULIP Plan's life insurance component might give financial assistance to dependents if an unexpected occurrence occurs before retirement. This keeps long-term family objectives from being completely undermined by unanticipated events.

Advantages for working professionals

For many professionals, retirement planning needs to fit around busy careers and everyday responsibilities. A ULIP Plan offers several features that support this requirement.

Factors to consider before choosing a ULIP Plan

A ULIP Plan should always be evaluated in relation to a person's overall financial plan.

● Financial objectives: Before making investment decisions, one should take into account the anticipated retirement age, lifestyle needs, future obligations, and retirement expenses.

● Risk appetite: While conservative investors might allocate more money to debt-oriented funds, investors who are at ease with market swings might want more equities of exposure.

● Investment duration: Long-term financial objectives are typically the focus of ULIPs. The intended retirement period and the investing horizon should coincide.

● Overall financial strategy: Provident funds, mutual funds, pension products, and other retirement-focused assets can be utilised in conjunction with a ULIP Plan. A more balanced financial foundation is frequently produced with the aid of a varied strategy.

Conclusion

Retirement planning involves patience, perseverance, and a thorough awareness of future financial demands. With longer life expectancies and shifting retirement expectations, more people are looking at a broader choice of investing options. A ULIP Plan has contributed to this transition by combining investment development potential with life insurance coverage. Solutions offered by insurers such as Tata AIA are part of the broader range of options available to investors seeking long-term financial planning and protection. It can make a significant contribution to a long-term retirement plan intended to maintain financial stability in later years, but it should be assessed alongside other financial products.