Higher education today is no longer a peripheral milestone. Whether domestic or global, it represents a future financial obligation that must be met at a specific point in time, irrespective of market cycles, interest rate environments, or personal circumstances. For Indian families planning a child’s higher education, safety often becomes the dominant lens through which savings decisions are made. But in this context, the question is not whether fixed deposits or savings plan are better, but whether they are structurally appropriate for the goal.

Why fixed deposits feel right and where they fall short

Fixed deposits continue to appeal because they deliver certainty of capital and a predictable interest stream. For short term allocations, emergency liquidity, or capital parking, they remain effective instruments. But what appears stable in isolation often proves insufficient when layered against rising tuition costs, currency exposure, and auxiliary expenses such as accommodation and living costs.

The limitation emerges when they are pressed into service for long horizon education planning. Over 12–18 years, fixed deposits are exposed to three structural weaknesses:

· Returns that rarely outpace education inflation

· Reinvestment risk across interest rate cycles

· Complete dependence on uninterrupted contribution discipline

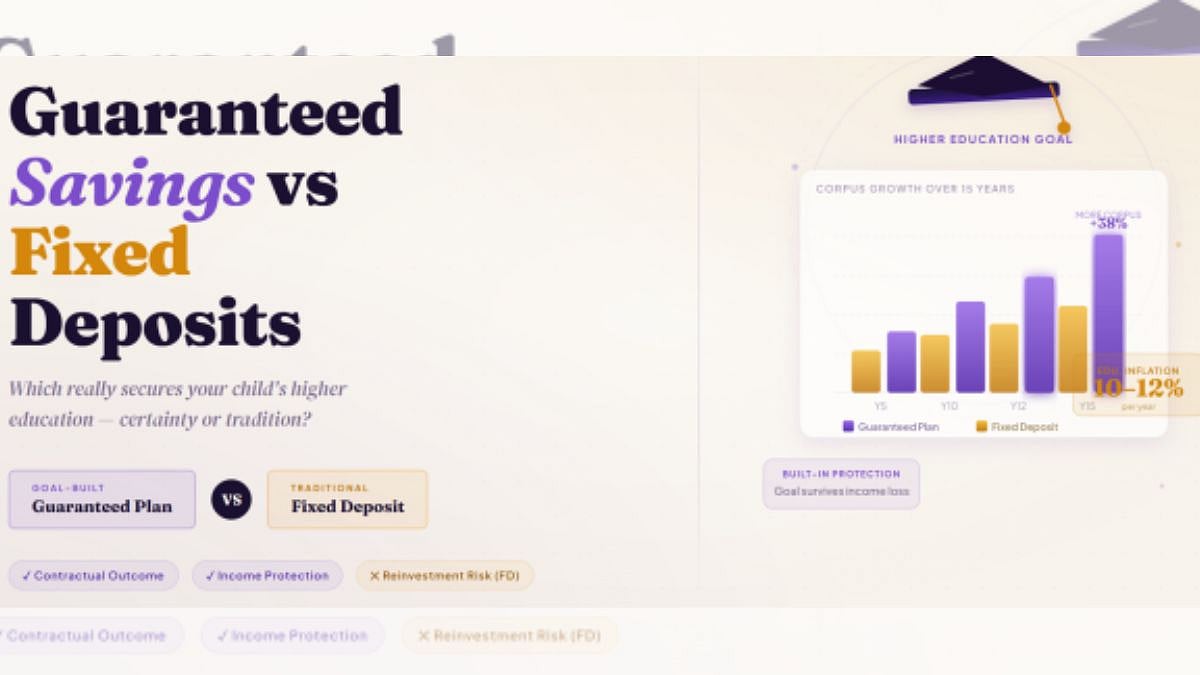

Guaranteed savings plans ensures certainty of outcomes

Guaranteed savings plans are not designed to replace all traditional saving instruments. They exist for delivering a known financial outcome on a known future date. Instead of relying on periodic renewal decisions and variable interest environments, these plans contractually define maturity benefits upfront. Contributions are structured, timelines are fixed, and outcomes are aligned to specific goals such as higher education.

This design philosophy explains why institutions like Kotak Life position guaranteed savings not as return seeking products, but as planning anchors within long term family strategies. Their value lies less in yield comparisons and more in outcome reliability.

The overlooked variable: income continuity risk

Most education savings calculations assume a stable income stream across the accumulation phase. This assumption is rarely challenged, yet it represents the single largest vulnerability in education planning Fixed deposits do nothing to address this risk. If income is disrupted, the entire saving strategy stalls.

Guaranteed savings plans through insurers such as Kotak Life address this structurally by embedding protection within the solution. In the event of an unforeseen earning loss, the plan either continues or pays out as defined, safeguarding the child’s education objective regardless of circumstances.

A disciplined comparison, not a superficial one

Consideration

Fixed Deposits

Guaranteed Savings Plans

Goal alignment

Generic

Goal specific

Inflation resilience

Limited

Structured

Income protection

None

Inbuilt

Reinvestment risk

High

Eliminated

Outcome certainty

Behaviour dependent

Contractual

Seen through this lens, the decision becomes less about preference and more about planning integrity.

It’s also important to note that guaranteed savings plans do not operate in isolation. Families often balance them with other instruments for different objectives.

For example:

· Guaranteed savings plans for education certainty

· Market linked investments for long term wealth growth

· Retirement plans to secure post career income

Providers such as Kotak Life structure their product portfolios with this separation in mind, allowing families to address education, protection, and retirement independently yet cohesively.

Closing perspective

Fixed deposits remain useful instruments but they are not education strategies. Guaranteed savings plans, when structured correctly, are built precisely for goals that cannot be postponed, downsized, or renegotiated later. That is why an increasing number of parents, are reassessing traditional approaches and choosing solutions aligned to the realities of modern education costs. In higher education planning, safety is not about avoiding risk. It is about ensuring certainty where it matters most.

Fixed deposits offer capital stability, but they are not structured for long term goal certainty. Over extended periods, reinvestment risk, interest rate cycles, and education inflation can significantly erode their effectiveness. For higher education, where timelines and amounts are non negotiable, this gap becomes critical.

Guaranteed savings plans eliminate rollover decisions, reduce reinvestment dependency, and protect the goal itself rather than just the capital deployed toward it. This structural certainty is what distinguishes them in education planning.

Most savings approaches assume uninterrupted income across 10–15 years. Guaranteed savings plans account for the possibility that this assumption may fail. By embedding protection, they ensure that education funding remains intact even if income is disrupted—something fixed deposits do not address at all.

No. They function best as a core education funding anchor, not a comprehensive financial solution. Many families continue to use fixed deposits for short term liquidity, while using guaranteed savings plans to ring fence education goals and separate them from day to day financial volatility.

Education inflation typically outpaces general inflation. Fixed deposit returns, especially post tax, often struggle to keep pace over long periods. Guaranteed savings plans address this by structuring maturity benefits that are aligned with future cost projections, not present day assumptions.

Education is a goal where failure has lasting consequences. Advisors therefore prioritise certainty over optionality. Insurers such as Kotak Life are frequently referenced because their guaranteed savings solutions are built with long duration liabilities and goal specific planning in mind, rather than short term return positioning.