Owning a sports bike in India is mostly linked with performance, accuracy and a huge financial expenditure. The excitement of riding also brings along the responsibility of safeguarding that investment through appropriate insurance coverage. Knowing how premium, Insured Declared Value (IDV) and add-ons interact within a comprehensive policy is important before purchasing a new bike insurance online.

All these factors have their own distinct role, but are highly connected when it comes to the cost and the extent of protection.

Understanding Comprehensive Bike Insurance

A comprehensive bike insurance policy will take care of both the third-party liabilities and damages to the insured vehicle. For sports bikes, in which the cost of repair and the specialised parts is usually higher, this coverage is especially important. It can cover accidental damages, theft and natural disasters.

However, the extent of this protection is not fixed. It is based on the calculation of the premium, the IDV and the add-ons.

What Is IDV and Why Does It Matter

The Insured Declared Value (IDV) is the current market value of the bike. It is the maximum amount that can be considered in case of a total loss or theft claim.

For sports bikes, the IDV is relatively high because of the high purchase price. This directly influences two important aspects-

● An increase in IDV results in increased premiums.

● A lower value decreases the premium, but can impact the claim value.

Depreciation is normally taken into consideration to calculate the IDV. The value decreases as the bike becomes older. This may reduce the amount of the premium. However, setting it too low might result in inadequate financial coverage in case of significant damage or loss.

The Role Of Add-Ons In Enhancing Coverage

Add-ons are additional covers that are optional and added on top of a typical comprehensive policy. For sports bike owners, these may offer an added financial consideration in certain circumstances.

Some of the add-ons that can be considered include-

● Zero Depreciation Cover- Helps minimise the effect of depreciation when making claims, especially when dealing with costly components.

● Engine Protection Cover- This cover may be applicable in situations where there is engine damage as a result of water intrusion or oil spills.

● Roadside Assistance- Provides assistance in breakdowns, and this can be useful for long-distance riders.

● Consumables Cover- Covers the engine oil, nuts, bolts and other consumables that are normally left out.

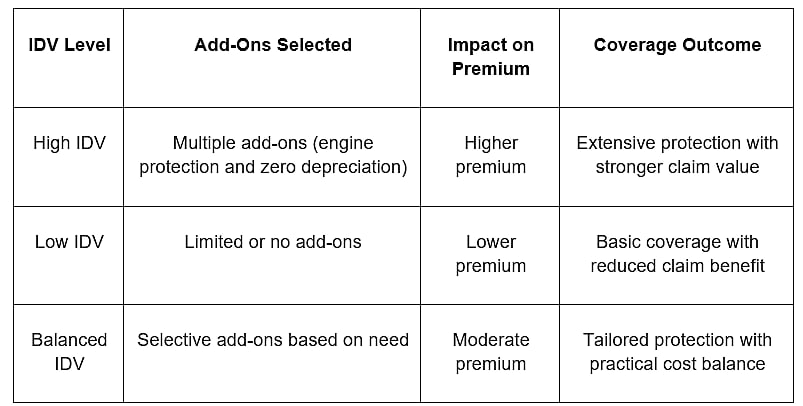

How Premium, IDV and Add-Ons Work Together

These three elements are interconnected. Adjusting one often impacts the others:

Choosing The Right Approach

It is essential to go beyond the typical or default settings and focus on what fits personal needs when assessing the option of new bike insurance online. Reviewing the policy frameworks helps in understanding how minor modifications can change the level of protection as well as the price.

Key Points to Consider

● Understand your usage pattern- Daily commuting, occasional use or long-range transportation all need varying amounts of coverage consideration.

● Choose IDV with balance- A moderate IDV will be enough to provide adequate claim value without increasing the premium.

● Select only relevant add-ons- Choose additional covers, such as engine protection or roadside assistance, only if they align with actual riding conditions.

● Compare policy structures before finalising- Reviewing multiple combinations helps in identifying the most suitable balance of cost and coverage.

● Focus on practical coverage value- The aim should be meaningful protection rather than simply choosing the lowest premium option.

Some insurance companies, including HDFC ERGO, offer structured policy benefits, in which some coverage elements can be modified.

Final Thoughts

Comprehensive new bike insurance online is not only a regulatory need, but also a viable factor for sports bike owners in India. Add-ons, premium and IDV are the basics of any policy. The balanced strategy will mean that the coverage is relevant to both the price of the bike and the way it is used.

Instead of only considering a cost, it is useful to review the connection between these elements to get a better outlook.