What is Monthly Investment Plan?

Monthly investment plans have often been perceived as investments in mutual funds, especially in the form of SIPs or Monthly Investment Plan SIP refers to the pre-planned investment in a mutual fund as fixed monthly instalments. The amount of investment is fixed and is automatically deducted from the investor’s account. The date of investment and number of months are decided beforehand.

Monthly Investment in ULIP

What many investors are not aware of is that it is possible to invest in a similar manner in Unit Linked Insurance Plans as well. ULIPs allow investors to invest in annual, quarterly, or monthly modes depending on their comfort.

Benefits of SIP in ULIPs

Monthly investment in ULIPs have multiple unique benefits since ULIP investments are tax exempt under section 80C:

Since the investment in ULIP is going to be tax deductible, it helps if you opt for an automated monthly saving to avoid last minute hassle every financial year.

Benefits of ULIPs over Mutual Fund Investments

ULIPs have multiple benefits over the mutual fund investments. However, two are the most important to note:

ULIPs are the only investments where you can enjoy both tax benefits and market linked returns from fixed income securities.

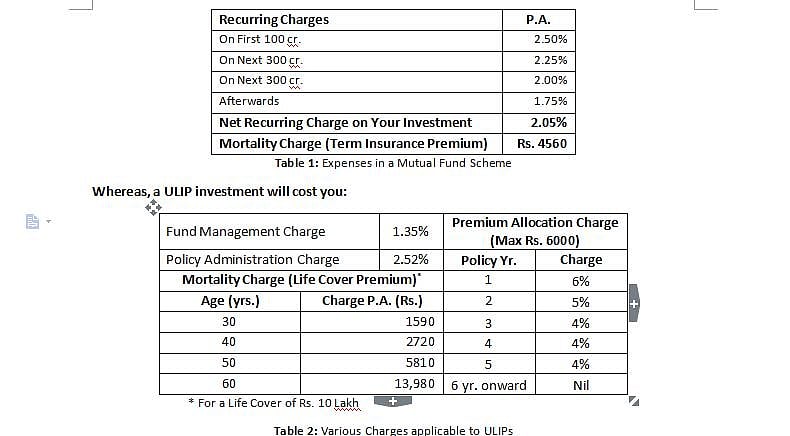

Cost Mutual Funds vs. ULIPs

ULIPs have been underrated for a long time citing high cost and lower liquidity offered by the earlier variants. However, now costs of investing in a ULIP is pretty much comparable and even lower in some cases from mutual funds (See the Cost Comparison Table below):

Assuming, you invest in a mutual fund which has a corpus (asset under management) of Rs. 1000 crore, and buy a pure term cover of Rs. 10,00,000…

A Mutual Fund Investment Will Cost:

It is understandable if you find these charges complicated. The ultimate effect of the various charges at different stages of investment can be calculated easily. Moreover, no doubt that ULIP has a greater number of charges to be deducted from your investment than a simple combination of Mutual Fund + Term Insurance.

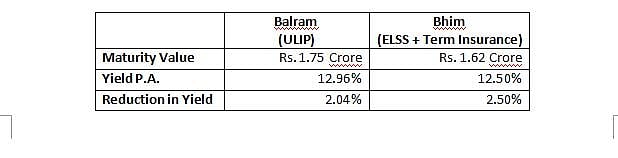

Effect on Returns Mutual Funds Vs. ULIPs

To understand the ultimate impact of the various charges on both mutual fund investments and ULIPs we estimated the returns based on the following scenario:

Two investors, Balram and Bhim, decide to invest in the following manner for the next 25 years, both are 30 years old now:

Balram chooses a ULIP Plan to invest his Rs. 100,000 and Bhim decides to go for a combination of tax saving mutual fund investment, ELSS (Equity Linked Saving Scheme) and e-term cover (online term insurance).

Here’s a result for both the investments, assuming the return on invested money had been 15% p.a. in the equity market for the 25-year period:

Table 2: Returns ULIP vs. Mutual Fund

Due to low recurring charges and mortality charge (life insurance premium) in the initial stages of the investment ULIP manages to earn a better return at the end of the 25 years’ period. However, with a mutual fund, the charges remain constant throughout life, and as the corpus builds up the amount of expense also goes up, resulting in lower maturity value.

How to Buy ULIPs?

Buying Unit Linked Plans is quite simple, once you have finalised the plan, and type of benefits you want to avail. You can contact the insurer directly who will send a representative to guide you through the application process.

The documents are delivered to your correspondence address once the policy has been issued.