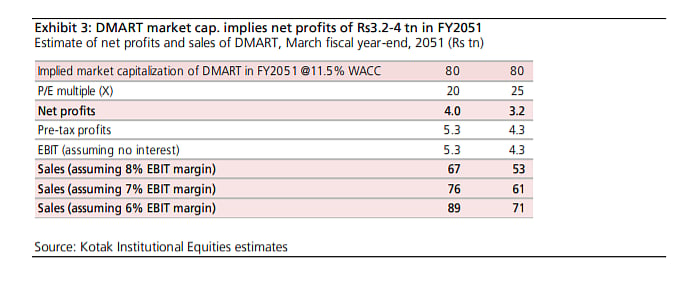

The market capitalization of DMart at Rs 3.2 trillion ($42 bn) would suggest that the market expects DMart's market capitalization to be around Rs 70-90 trillion by FY2050 when India’s GDP per capita will reach China’s current GDP per capita of $11,000.

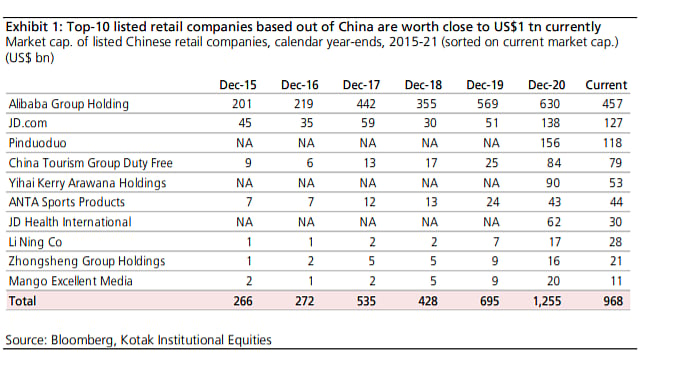

The three largest Chinese retailing companies (largely e-commerce) have a combined market capitalization of $0.75 trillion (Rs 55 trillion) currently; they have other businesses too.

Market is super-optimistic on DMart’s growth

DMart’s current market capitalization of Rs 3.2 trillion ($42 billion) will imply a market capitalization of Rs 70 trillion using a WACC of 11 percent and market capitalization of Rs 90 trillion using a WACC of 12 percent by FY2051.

India’s GDP per capita will reach China’s current GDP per capita by then. The top10 Chinese retailing (largely e-commerce) companies have a combined market capitalization of $1 trillion (Rs 75 trillion).

Top-10 listed retail firms based out of China | Kotak Institutional Equities

We note that some of them have other businesses, the value of which reflects in their overall market capitalization. It appears that the market is very confident of

1) strong growth in India’s GDP for the next several years,

2) large retailing market opportunity in terms of revenues and profits, and 3) flawless execution on part of DMart.

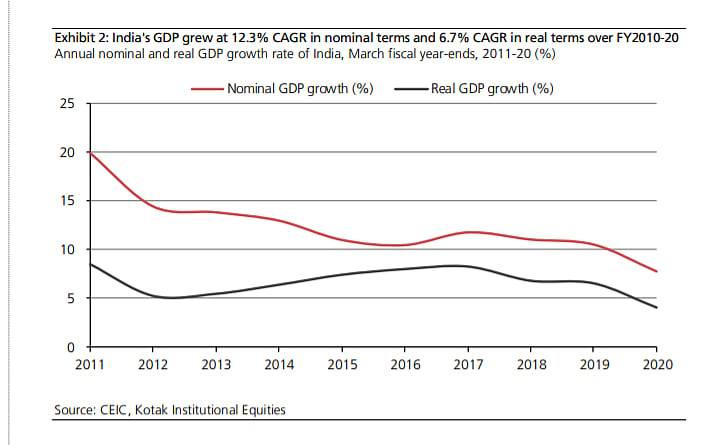

Assumption #1: India will reach China’s current GDP per capita in about 30 years

This is feasible if India’s GDP was to grow at 7 percent and its GDP per capita was to grow at 6 percent per annum. China’s GDP per capita is currently $11,000 and India’s $2,000. India’s GDP per capita will be about 5.5X if it was to compound at 6 percent for 29 years. We note that India’s GDP has grown at an average rate of 6.7 percent over FY2011-20

India's GDP grew at 12.3% CAGR in nominal terms | Kotak Institutional Equities

We are hopeful about acceleration in India’s GDP growth on the back of economic reforms and a multi-year investment cycle, which could result in a virtuous cycle of investment and consumption.

Assumption #2: Retailing market will present a large and profitable opportunity

A simple analysis shows that DMart would have to reach sales of around Rs 70 trillion, EBIT of Rs5.3 trillion and net profits of Rs 4 trillion in FY2050 to justify today’s market capitalization. We use a 20X P/E multiple for DMart in FY2051, which seems reasonable in the context of the ‘mature’ state of India’s economy and retailing market by then.

DMart market cap implications | Kotak Institutional Equities

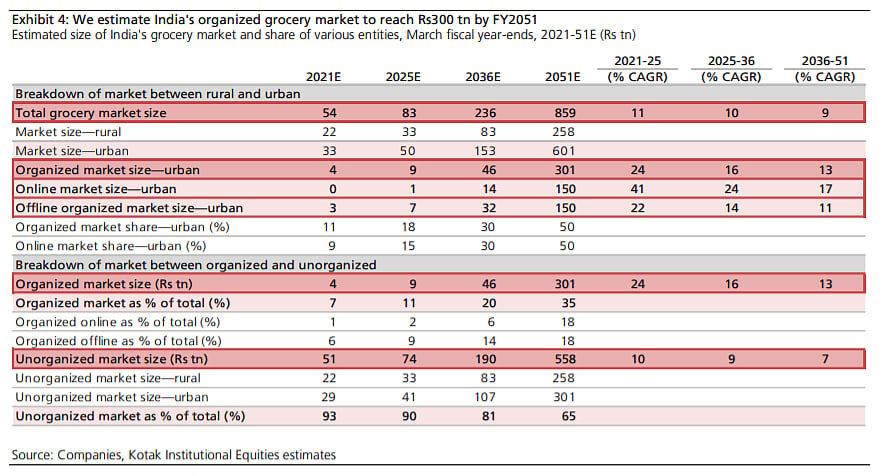

Our grocery market forecasts for FY2051 suggest that DMart would have to achieve 8 percent market share of India’s total grocery market, 12 percent of India’s urban grocery market and 23 percent of India’s formal urban grocery market.

Estimate of India's organized grocery market by FY2051 | Kotak Institutional Equities

We assume 45 percent of India’s population and 30 percent of consumption will be in rural markets in FY2050, which will largely be outside the purview of formal retailing. The share of rural population in China’s total population is about 35 percent currently.

Assumption #3: Flawless and superior execution versus several other competitors

The current market capitalization also implies rapid expansion of DMart’s digital and physical infrastructure that will enable it to meet the implied revenue and profit numbers (if not higher) for FY2050. We are not sure how to convert the implied FY2050E revenues into digital and physical infrastructure since the mix of offline and online retailing is a big variable.

(All of the views expressed in this report accurately reflect his or her personal views --Sanjeev Prasad, Anindya Bhowmik and Sunita Baldawa--about the subject companies and securities)