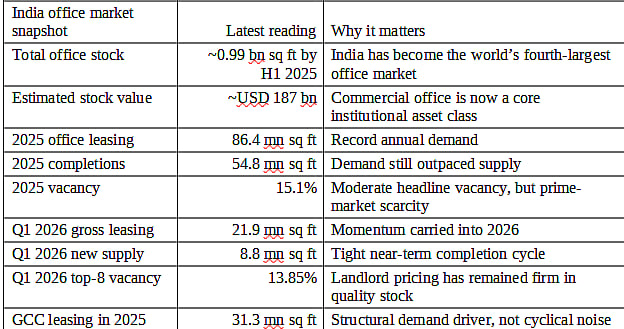

India’s office market has crossed an important threshold: it is no longer merely a low-cost outsourcing location, and it is no longer a “post-pandemic recovery” story. It has become a strategic operating platform for global enterprises. Knight Frank’s 2025 office supply study places India’s office stock at roughly 0.99 billion sq ft by H1 2025, making it the fourth-largest office market globally by area, with an estimated stock value of about USD 187 billion.

The same firm’s H2 2025 market report shows that office leasing reached a new record of 86.4 million sq ft in 2025, while completions were 54.8 million sq ft and vacancy settled at 15.1% across the tracked markets. In Q1 2026, Cushman & Wakefield still recorded a healthy 21.9 million sq ft of gross leasing and 8.8 million sq ft of new completions across the top eight cities, with average office vacancy tightening to 13.85%. In other words, demand remains ahead of supply in quality stock, and the market has retained momentum even as global uncertainty has increased.

The single most important demand engine is the Global Capability Centre. JLL says GCCs leased 31.3 million sq ft in 2025, accounting for 38% of office leasing across India’s top seven cities, while ICRA notes that India hosts about 1,700 GCCs today and could exceed 2,500 by 2030, with USD 100 billion-plus in sector revenue and 50–55 million sq ft of additional Grade A office demand across FY2026–FY2027.

JLL also highlights that more than 90% of current GCC activity remains concentrated in Tier I cities and already occupies 263+ million sq ft of Grade A office space, but the same report makes a point that is central to my investment thesis: Tier II and secondary cities can offer 10–35% cost savings versus major metros, provided talent, infrastructure, and operating ecosystems are credible.

That is why I would split India’s opportunity into two distinct but connected plays. The first is the high-liquidity, institutionally deep Tier I market, where the focus should be on transit-rich Grade A and A+ assets, campus formats, redevelopments, and ESG-led rental resilience.

The second is the selective, policy-assisted affordable-hub strategy, where cities like Indore, Thiruvananthapuram, Jaipur, Kochi, Lucknow, Surat, and Visakhapatnam can compete not by imitating Bengaluru or Gurugram, but by becoming specialised satellites for GCCs, digital operations, engineering support, non-core back-office, or hybrid distributed teams.

However, I want to be explicit about one analytical limitation: unlike the six major metros, most Tier II cities do not yet have consistently published, institutional quarterly rent, vacancy, and supply series from the large brokers. For those markets, the evidence base is strongest on policy, park-level supply, anchor occupiers, and infrastructure, and weaker on citywide rental precision.

My bottom-line view is straightforward. Over the next three to five years, India’s office winners will not be determined by nominal rent alone. They will be determined by the combination of talent density, transport connectivity, Grade A stock quality, ESG compliance, policy execution, and the ability to offer flexible yet scalable lease structures. Cities that can combine these factors will capture the next wave of GCCs and premium domestic occupiers; cities that only offer cheap land will struggle to monetise supply.

National market architecture

The national story is now one of scale, quality, and scarcity within the right product band. Knight Frank’s “A Billion sq ft and Counting” report shows office stock rising from 192 million sq ft in 2005 to about 993 million sq ft by H1 2025, a 20-year CAGR of 8.6%.

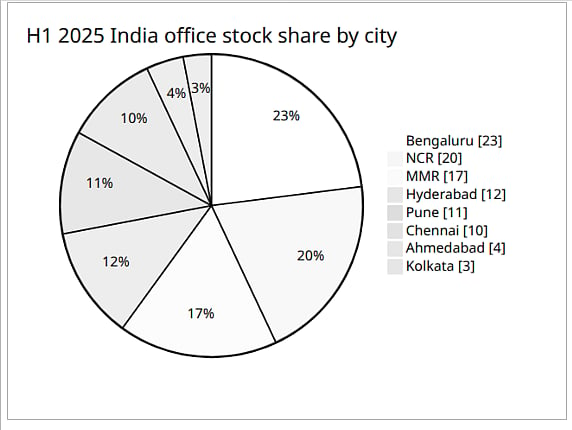

Stock remains highly concentrated: Bengaluru, NCR, and MMR together account for 60%, while Hyderabad, Pune, and Chennai contribute another 33%, leaving only 7% for Ahmedabad and Kolkata in that tracked universe. This concentration matters because it explains why liquidity, investment, and occupier trust remain strongest in a handful of corridors even when India-wide leasing is booming.

Just as important is the grade mix. Knight Frank estimates that, on average, 53% of key-city office stock is now Grade A, 43% is Grade B, and just 4% is Grade C. Bengaluru, Hyderabad, and Chennai lead in Grade A share, while older markets such as MMR and NCR still carry larger stocks of legacy Grade B inventory. That is the clearest explanation for the divergence now visible in India: prime assets continue to lease, escalate rents, and attract institutional money, while under-specified secondary buildings increasingly face obsolescence risk.

This quality bifurcation is reinforced by Knight Frank’s finding that Grade A assets dominated 91% of annual transactions in 2025, while JLL and ICRA both highlight occupier preference for integrated, green-certified, tech-enabled campuses.

The supply–demand math also supports a constructive medium-term view. Knight Frank’s long-cycle analysis shows India’s office completion-to-absorption ratio collapsing from 1.40 in 2008 to just 0.41 in H1 2025, which is another way of saying the supply pipeline has become more disciplined than in prior cycles.

In full-year 2025, transactions of 86.4 million sq ft significantly outpaced completions of 54.8 million sq ft. Even with some market-specific softness and periodic spikes in new delivery, the national balance still favours landlords in prime assets. Cushman & Wakefield’s Q1 2026 data is consistent with this interpretation: new supply fell to a seven-quarter low of 8.8 million sq ft, vacancy compressed, and rents continued to rise.

Rents tell the same story. Knight Frank’s H2 2025 rent table shows major-city transacted rents ranging from about ₹44 psf/month in Ahmedabad to ₹125 psf/month in Mumbai, with Delhi NCR and Hyderabad each posting 10% year-on-year rent growth, followed by Mumbai and Bengaluru at 6%. ICRA adds a useful global lens: India’s prime office rentals remain among the most affordable globally at roughly USD 1–2 per sq ft per month, which is one reason GCC economics remain attractive even when wages and fit-out standards improve.

To make that affordability tangible, I use a simple, transparent metric in this report: the Rental Affordability Index, defined as Mumbai’s 2025 transacted rent divided by the target city’s rent, with Mumbai = 100. A higher score means a lower rental burden relative to Mumbai.

This is not a wage-linked affordability metric; it is a pure rent-cost comparator. It matters because for occupiers expanding across India, the first pass of location strategy is usually not “which city is cheapest?” but “which city gives me acceptable quality at a significant discount to my highest-cost benchmark?”

The market-share chart above is based on Knight Frank’s H1 2025 office stock study and captures why capital, leasing depth, and pricing power remain concentrated in a few cities.

The market-share chart above is based on Knight Frank’s H1 2025 office stock study and captures why capital, leasing depth, and pricing power remain concentrated in a few cities.

The national snapshot draws on Knight Frank’s 2025 office-stock and H2 2025 market reports, JLL’s 2026 GCC analysis, ICRA’s GCC thematic report, and Cushman & Wakefield’s Q1 2026 office report.

Major metro market profiles

For the six principal metros, the evidence is strong enough to compare stock, leasing, vacancy, rents, and very near-term supply using a common framework. The key point is that India’s office cycle is not monolithic. Bengaluru remains the deepest technology-and-GCC market. Delhi NCR combines large demand pools with significant new supply and rising GCC share. Mumbai leads current-quarter leasing and remains the country’s capital-market gateway, though at the highest rental point. Hyderabad and Chennai are the most convincing “quality at a discount” stories among Tier I cities. Pune is increasingly a serious GCC co-leader rather than just a spillover market from Mumbai.

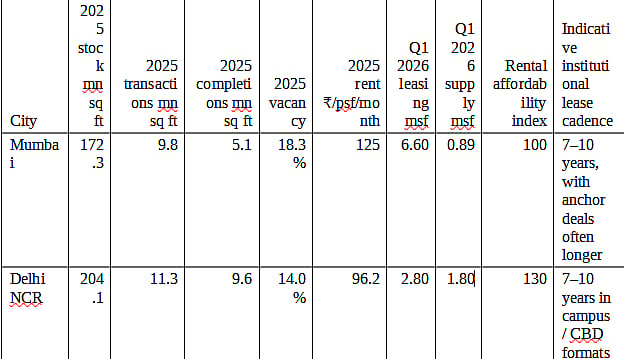

The 2025 stock, transactions, completions, vacancy, and rents come from Knight Frank’s H2 2025 city market summaries; Q1 2026 leasing and supply come from Cushman & Wakefield. The Rental Affordability Index is my calculation using Mumbai’s 2025 transacted rent as the benchmark. Lease-cadence ranges are indicative, inferred from public REIT lease examples, disclosed WALEs, and large registered transactions rather than from a broker-published city average.

Mumbai. Mumbai remains the highest-rent office market in India at around ₹125 psf/month, with a large stock base of 172.3 million sq ft and relatively elevated vacancy at 18.3% because the metropolitan market includes a wider range of submarkets and some structural decentralisation. Yet the city led India’s Q1 2026 leasing at 6.6 million sq ft, accounting for about 30% of pan-India activity in that quarter. The centre of gravity is no longer only traditional CBD/BKC; large-format users have increasingly favoured Andheri East, Goregaon, Airoli, and Thane, which offer scale. That is why I view Mumbai as a two-speed market: premium core locations remain strategic and scarce, while suburban and Navi-Mumbai corridors have become the real scale engine for BFSI, technology support, data, and managed-office demand. Institutional capital still treats Mumbai as the gateway market: Cushman & Wakefield reported more than USD 1.2 billion of institutional real estate investment in Jan–Sep 2025, and Maharashtra’s GCC policy now seeks to attract 400 new GCCs and 400,000 skilled jobs over time.

Delhi NCR. NCR has become a more sophisticated office market than many still assume. Its 2025 leasing reached 11.3 million sq ft, while the stock base is already 204.1 million sq ft. Vacancy at 14% rose because completions were very strong, but Knight Frank’s city commentary is clear that premium micromarkets such as DLF Cyber City, Golf Course Road, and Connaught Place are operating at sub-10% vacancy, which is exactly why citywide averages can be misleading. Just as important, GCCs are now a meaningful demand driver: Knight Frank says their share of NCR transactions rose from 19% in 2024 to 26% in 2025. Infrastructure is also a real differentiator here rather than a talking point; Knight Frank highlights the new 28.5 km Gurugram Metro proposal and two additional sanctioned corridors that would deepen connectivity between established corporate districts and older urban fabric. In my reading, NCR is the most convincing large-scale corporate services market in India after Bengaluru, especially for diversified users spanning IT, BFSI, consulting, e-commerce, healthcare, and shared services.

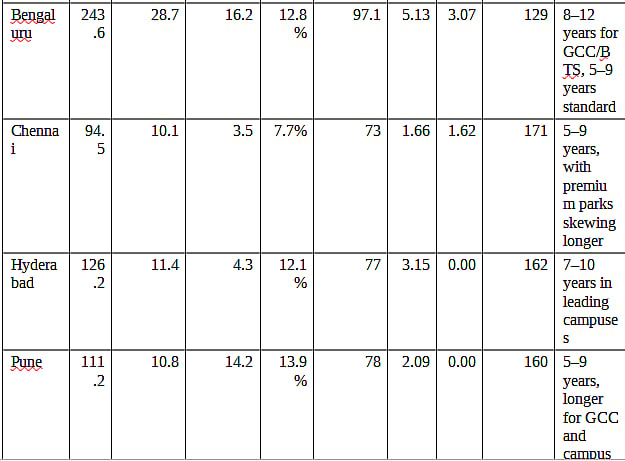

Bengaluru. Bengaluru is still the country’s benchmark office market. Knight Frank puts its 2025 stock at 243.6 million sq ft, vacancy at 12.8%, and annual leasing at a remarkable 28.7 million sq ft; that made it the largest office market by both stock and absorption in the country. Knight Frank’s India narrative also notes that around 43% of Bengaluru’s annual volume was pre-committed, which tells me occupiers are willing to lock in premium future-ready space before delivery when the right asset comes to market. JLL says Bengaluru now hosts 900+ GCC units and commands 34–39% of national GCC activity, with strengths across technology, ER&D, BFSI, innovation, and retail operations. The REIT and developer evidence lines up with that story: Embassy REIT’s portfolio is overwhelmingly Bengaluru-led, and Embassy TechVillage remains one of the flagship integrated campuses in the Outer Ring Road corridor. In practical terms, Bengaluru is the least replaceable office city in India today—not because it is cheapest, but because it is deepest.

Chennai. Chennai looks increasingly compelling to me because it combines Tier I depth with Tier II-style discipline on costs. Knight Frank’s numbers show a relatively low 7.7% vacancy, a stock base of 94.5 million sq ft, and 2025 rents of roughly ₹73 psf/month, well below Bengaluru, NCR, and Mumbai. The occupier mix is changing in an important way: Chennai is no longer just an IT/ITeS city. Knight Frank highlights major occupiers such as Optum, Qualcomm, Schneider Electric, Hitachi Energy, and BMW, while JLL positions Chennai as India’s manufacturing-and-automotive GCC hub with complementary IT, BFSI, and ER&D strengths. Even in Q1 2026, Chennai registered 1.66 million sq ft of leasing and 1.62 million sq ft of supply—essentially a balanced quarter. If I were building a medium-cost GCC or engineering-support strategy today, Chennai would be one of the first cities I would underwrite because it offers a rare combination of talent depth, industrial adjacency, and rental efficiency.

Hyderabad. Hyderabad’s 2025 numbers are some of the strongest in the country: 11.4 million sq ft of transactions, only 4.3 million sq ft of completions, a vacancy rate of 12.1%, and rents of about ₹77 psf/month after 10% annual growth. Its strategic identity is also now much clearer. JLL calls Hyderabad the country’s healthcare-biotech leader, with 20–23% of India’s GCC market, and the city’s 2025 office performance was supported by major occupiers such as Charles Schwab, Warner Bros. Discovery, Randstad, Goldman Sachs, and ServiceNow. Knight Frank attributes part of Hyderabad’s residential and office resilience to metro expansion and ring-road connectivity, and that matters because the city’s office geography is still being steadily improved rather than compressed. For me, Hyderabad is no longer primarily a challenger to Bengaluru; it is a fully institutionalised, lower-cost premium market in its own right.

Pune. Pune has quietly moved into the top tier of India’s office conversation. Knight Frank shows 111.2 million sq ft of stock, 10.8 million sq ft of 2025 transactions, and 14.2 million sq ft of completions, which pushed vacancy to 13.9% and kept rent growth modest at 1% to around ₹78 psf/month. On the surface that looks like a supply-heavy market, but the demand quality is what matters: Knight Frank says third-party IT/ITeS accounted for 31% of H2 2025 leasing, GCCs 27%, and flex 21%. JLL further says Pune captured 15–20% of national GCC activity over the past four years and has become especially strong in BFSI, automotive, IT/ITeS, manufacturing, and engineering services. My reading is that Pune’s near-term challenge is absorption of recently delivered stock, but its medium-term advantage is the breadth of occupier logic. It is neither purely a spillover market nor only a cheaper alternative to Mumbai. It is becoming its own platform city.

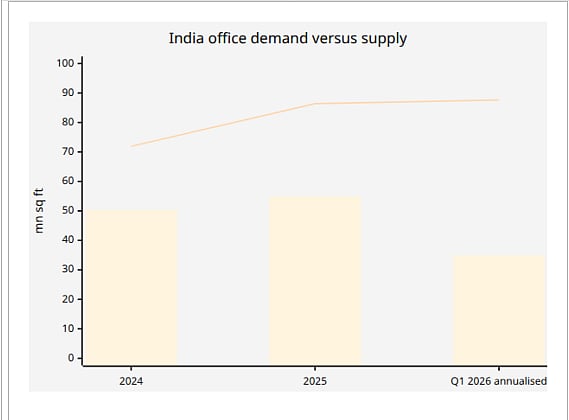

The chart above uses Knight Frank’s full-year 2024 and 2025 transaction data, Knight Frank’s 2025 completion data, and an annualised run-rate from Cushman & Wakefield’s Q1 2026 leasing and supply numbers. It illustrates the central fact of the cycle: India is still consuming quality office faster than it is producing it.

For emerging hubs, I want to state the methodology clearly before I get into city reads. Unlike the six major metros, institutional, quarterly, citywide rent and vacancy series are not consistently published for most Tier II markets. JLL’s 2026 GCC guide, however, is explicit that secondary cities now offer 10–35% cost savings and are turning into “sophisticated business hubs” where the business case is no longer only cost arbitrage, but a mix of cost, talent, resilience, and policy support. So in these markets, I prioritise park-level supply, anchor tenants, government facilitation, transport upgrades, and GCC readiness over false numerical precision. Ahmedabad is the exception because it is already present in the national broker databases.

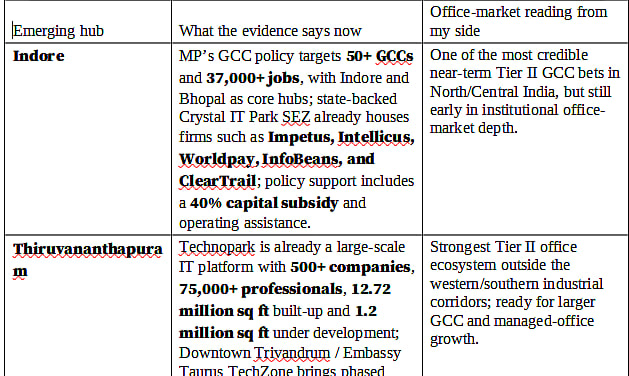

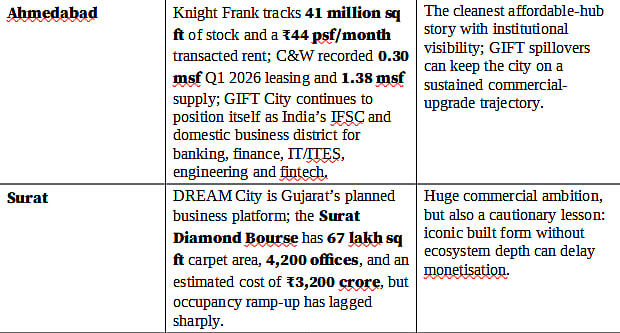

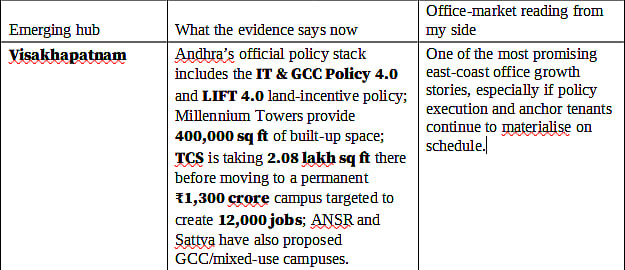

The emerging-hub comparison above draws from JLL’s national GCC guide, official and quasi-official park sources, state policy summaries, and recent investment announcements. It is intentionally stronger on supply, policy, and occupiers than on citywide rent/vacancy precision, because that is where the current evidence base is strongest.

Indore. Indore is the city I would watch most closely in the central Indian Tier II group. The state’s GCC policy explicitly positions Indore and Bhopal as core hubs and aims for 50-plus GCCs and 37,000-plus jobs. The state-backed Crystal IT Park / Crystal IT Park SEZ already shows that the city’s office story has moved beyond aspiration: official and semi-official listings name occupiers such as Impetus, Intellicus, Worldpay, InfoBeans, and ClearTrail. The important point is not that Indore is suddenly a metro-scale market; it is that the city now has the ingredients for a targeted GCC proposition—lower operating costs, a visible tenant base, and direct subsidy support through the GCC policy. Public citywide rent and vacancy benchmarks remain sparse, so I would treat Indore as a selective, early-stage institutional bet, not yet a fully benchmarked office market.

Thiruvananthapuram. Among affordable hubs, Thiruvananthapuram has the strongest combination of existing technology scale and future premium office pipeline. Technopark’s public profile points to 500-plus companies, 75,000-plus professionals, 12.72 million sq ft of built-up space, and more than 1.2 million sq ft under development. The Downtown Trivandrum / Embassy Taurus platform brings something even more significant: institutional mixed-use office development at scale, including large SEZ office stock, non-SEZ office, retail, hotel, and residential components. Technopark is also now offering Phase IV land on long leases to private developers, which is a meaningful signal that the market is ready to widen its developer base. In my view, Thiruvananthapuram is no longer only a Kerala IT-park story; it is becoming a genuine alternative location for scaled technology, BFSI support, and internationally oriented GCCs.

Jaipur. Jaipur’s commercial proposition still works best when seen through the lens of Mahindra World City Jaipur rather than through conventional CBD office metrics. The project is a large PPP between Mahindra and RIICO, spans 3,000 acres, and offers a rare SEZ + DTA framework in one integrated business city. The official tenant list includes Infosys, Deutsche Bank, MetLife, Amazon, Flipkart, JCB, and others. Its official positioning inside the Delhi–Mumbai Industrial Corridor influence zone is important because Jaipur’s long-term commercial logic depends on corridor connectivity and industrial-services adjacency. The caveat is equally important: recent reporting shows that the export-oriented SEZ model has lost momentum since older SEZ tax advantages tapered, and the project has sought greater domestic-use flexibility. So Jaipur remains investable, but the investment case is strongest where occupiers want a campus-style, lower-cost North India operating base rather than a pure central-office address.

Kochi. Kochi’s office story is less about a single landmark tower and more about the strength of a government-backed IT ecosystem that is adapting intelligently to hybrid work. Infopark’s official platform already offers both SEZ and non-SEZ infrastructure, plug-and-play facilities, and land options, and recent local reporting shows meaningful demand for metro-linked distributed work formats such as “i by Infopark” at Ernakulam South. That matters because Kochi is especially well-suited to the next stage of India’s office market, where not every employee, team, or function needs to be concentrated inside one mega-campus. I see Kochi as a practical hub-and-spoke city, with relevance for managed offices, hybrid teams, and selected GCC support functions willing to trade some depth for lower cost and good liveability.

Lucknow. Lucknow is a policy-led story today rather than a fully institutional office-market story. Uttar Pradesh’s GCC policy is unusually broad in scope, covering lease, power, cloud, payroll, internships, skill development, land, stamp duty, and EPF reimbursements, and the state says it intends to create around 200,000 jobs through the policy. That is a serious signal, and it matters because Lucknow has administrative, educational, and healthcare gravity that could support service-sector expansion. But I would be cautious about over-underwriting the city before deeper private-sector office infrastructure emerges. Public citywide office stock, rent, and vacancy data are not yet robust enough to justify metro-style assumptions.

Ahmedabad. Ahmedabad is the most institutionally legible affordable market after Pune and Chennai. Knight Frank already tracks 41 million sq ft of office stock and a rent of about ₹44 psf/month, and C&W recorded 1.38 million sq ft of new supply in Q1 2026. The city’s strongest structural differentiator is GIFT City, which formally positions itself as India’s IFSC and a smart-city business district for banking, capital markets, insurance, IT/ITES, engineering, fintech, and even global in-house centres. Recent leasing activity by flexible workspace operators in the Ahmedabad–GIFT corridor suggests the ecosystem is deepening. I would treat Ahmedabad as a market where the affordability story is already visible and the institutionalisation curve is moving faster than most Tier II peers.

Surat. Surat’s commercial narrative is dominated by DREAM City and the Surat Diamond Bourse, and that makes it fascinating but also cautionary. On paper the bourse is enormous—67 lakh sq ft of carpet area, 4,200 offices, and a cost of around ₹3,200 crore. In practice, occupancy ramp-up has been slow. For me, Surat is the clearest reminder that commercial real estate needs more than a large building and a famous sectoral anchor. It needs air connectivity, business migration, service ecosystems, finance, and surrounding urban support. Over time, DREAM City may still succeed as a broader commercial district, but near-term underwriting in Surat needs to be conservative.

Visakhapatnam. Visakhapatnam is one of the most interesting expansion markets on the east coast because the state’s policy architecture and anchor-tenant pipeline are both visible. Andhra Pradesh’s policy stack now includes an explicit IT & GCC Policy 4.0 and the LIFT 4.0 land-incentive framework, while Millennium Towers already provide around 400,000 sq ft of office stock in the city’s IT district. The TCS story is especially important: it is taking 2.08 lakh sq ft in Millennium Towers before moving into a permanent ₹1,300 crore campus that the state expects to generate 12,000 jobs. Add to that ANSR’s proposed GCC innovation campus and Sattva’s mixed-use proposal, and Vizag begins to look less like a speculative hope and more like a credible medium-term office market in formation.

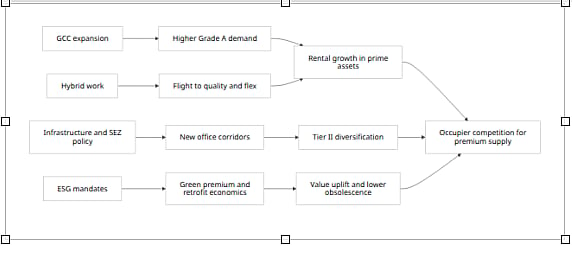

The biggest structural driver is still GCC growth, but it is important to understand why GCCs are now different from the old “captive centre” model. JLL’s 2026 GCC guide says India hosts 2,000-plus GCCs employing 1.9 million-plus professionals, and these centres now span AI, R&D, analytics, digital transformation, finance, and mission-critical operations rather than just transactional back-office work. ICRA’s 2025 report reinforces that point by noting that GCCs are moving into product development, AI/ML, cloud, and digital transformation, and that US-based GCCs accounted for 70% of total GCC absorption since 2021. The office implication is profound: these occupiers want quality, resilience, security, ESG credentials, and long-term growth pathways, not only low rent.

The second major driver is the changing relationship between remote work, hybrid work, and physical office strategy. Academic research internationally has shown that rising work-from-home adoption can reduce office valuations, raise vacancy, and slow development—especially for commodity buildings and weaker locations. But India’s market outcome has been more segmented than uniformly negative. Knight Frank, JLL, and C&W all show strong leasing persistence in premium office product, while flexible workspace demand has accelerated. Knight Frank recorded about 18.6 million sq ft of flex absorption in 2025, and C&W says flex operators still captured 18% of Q1 2026 leasing. The implication I draw is that hybrid work has not “killed” the Indian office; it has raised the premium on the right office and accelerated the decline of the wrong one.

The third driver is simple but powerful: India still has a compelling global cost proposition. ICRA explicitly says India’s prime office rents are among the world’s most affordable at USD 1–2 psf/month, while JLL argues that secondary markets can reduce costs by 10–35% further. In a world where occupiers are trying to build redundancy into their portfolios without giving up quality, that combination matters enormously. It means India can simultaneously support premium Grade A growth in Tier I markets and selective decentralisation into credible Tier II locations. That is exactly why I think the next cycle will be more distributed than the last one, even if Tier I cities still dominate absolute leasing volumes.

Infrastructure and policy have become much more central to office-market performance than they were a decade ago. Knight Frank’s supply-growth study explicitly links the evolution of India’s office market to GST reform, PM Gati Shakti, the National Logistics Policy, metro and transport expansion, and PPP-led urban development. On the ground, this translates into corridor creation: Gurugram metro expansions in NCR, metro-linked corridors in Chennai, better ring-road and metro connectivity in Hyderabad, DMIC-linked business geographies in Jaipur, and land-incentive or GCC-targeted frameworks in MP, UP, and Andhra Pradesh. In my view, the smartest investors are no longer buying “city stories”; they are buying corridor stories inside cities and policy-plus-corridor stories outside them.

ESG is no longer optional, and the academic and market evidence now align on that point. A 2024 India-focused academic paper that analysed over 17,000 office rental contracts found that green and healthy office labels in India commanded rental premiums of 4–21%. JLL separately reported an average green premium of 7.1% across eight major Indian office markets, and ICRA noted that 65% of new GCC leasing is happening in green-certified integrated tech parks. Knight Frank’s retrofitting analysis goes even further, arguing that strategic retrofits can compress vacancy below 5% and boost asset values by 40–60%. For me, that means ESG is no longer a reporting layer; it is core underwriting logic.

The diagram captures my reading of the current cycle: multiple structural drivers are converging on the same outcome—premium, connected, sustainable space is gaining pricing power, while secondary, undifferentiated stock is losing it.

Indore case study — Crystal IT Park and the MP GCC push. The most instructive thing about Indore is not one trophy tower; it is how a state-backed IT-park base is being upgraded into a GCC proposition. Official/semi-official records for Crystal IT Park SEZ show occupiers such as Impetus, Intellicus, Worldpay, InfoBeans, and ClearTrail, proving that the city already has a functional digital-services cluster. The MP GCC Policy 2025 then tries to convert this cluster into a sharper investment proposition by targeting 50+ GCCs, 37,000+ jobs, and offering a 40% capital subsidy plus additional support on skills, IP, and operations. From a developer-strategy standpoint, this is the classic Tier II playbook: start with lower-cost plug-and-play or park-based inventory, then use policy support to pull in captive centres and mid-scale global users. Public lease documents are not yet rich enough to establish a reliable citywide rent series or lease-term average, so the financial metric that matters most at this stage is not blended rent but effective cost reduction via subsidy. For occupiers, that can materially alter feasibility. For investors, it also means the city remains policy-sensitive; execution quality will matter as much as real estate itself.

Thiruvananthapuram case study — Embassy Taurus TechZone and Downtown Trivandrum. This is one of the better examples in India of a Tier II city being upgraded through institutional mixed-use development. Technopark’s Taurus-led development pipeline includes large SEZ and non-SEZ office components, while official sources describe the broader Downtown Trivandrum project as including substantial IT office area, retail, hospitality, and serviced residences. The Niagara building alone offers 1.5 million sq ft and has already hosted major occupiers, while Embassy Taurus also created Keystone, a 62,500 sq ft prefabricated plug-and-play incubation space so tenants can start operations before permanent fit-outs are ready. That is a smart developer strategy because it attacks one of the biggest frictions in new office markets: time-to-occupy. The city also recorded what was described as Kerala’s largest single office lease when Allianz took 463,704 sq ft in the project ecosystem. The lease structure here is shaped by long-tenure SEZ demand plus phased non-SEZ mixed-use monetisation, and the financial value lies in phasing, diversification, and early anchor capture, not in chasing short-term headline rents.

Jaipur case study — Mahindra World City Jaipur. Jaipur’s strongest commercial case study is still Mahindra World City Jaipur, and it matters because it shows both the strengths and the limits of integrated office-industrial urbanisation. Officially, the project covers 3,000 acres, with 1,500 acres of SEZ, 1,000 acres of DTA, and a planned social/residential component, and hosts occupiers ranging from Infosys and Deutsche Bank to MetLife, Amazon, Flipkart, and JCB. The developer strategy is different from a standard rent-yield office model: this is an integrated business-city monetisation strategy built on land allotment, ecosystem formation, corridor access, and ESG positioning. Mahindra’s official materials emphasise sustainability and require operating savings in buildings relative to conventional stock; older climate-roadmap material also points to meaningful energy savings at the on-site IT park. But recent reporting also shows the challenge: after the tapering of older SEZ tax benefits, the export-led part of the proposition lost some momentum and the project has sought more domestic-use flexibility. The lesson, in my view, is that Jaipur can work very well for lower-cost North India corporate operations, but its monetisation is strongest when it is treated as a multi-use operating district, not when it is judged against Gurgaon’s office towers.

Bengaluru case study — Embassy TechVillage. Embassy TechVillage shows what a mature Indian campus strategy looks like when done properly. Embassy’s official portfolio page describes it as an 84-acre integrated office park in Bengaluru’s Outer Ring Road corridor, with 40+ occupiers, around 45,000 employees, and 88% of gross rentals derived from multinationals. That rent mix is critical because it creates durable cash flow and supports high-quality asset management. Embassy’s strategy at ETV has long combined large-format leasing, built-to-suit capability, and campus amenities. A prior official Embassy press release described a 1.1 million sq ft built-to-suit commitment for J.P. Morgan at the campus, while more recent market reporting shows Intuit signing a ₹915 crore lease for over 630,000 sq ft in 2026. The lease structure here is exactly what high-grade Indian office should aspire to: long-duration, multinational-backed commitments tied to a scalable campus with integrated services. Financially, ETV demonstrates the compounding value of institutional grade—high MNC rental share, repeated anchor expansions, and the ability to keep leasing even when broader markets wobble.

Gurugram case study — Atrium Place and the DLF-Hines model. Atrium Place is a good case study because it reflects the mature end of NCR’s premium office market. DLF’s official project page describes this joint project with Hines as a 3.07 million sq ft Grade A+ development on nearly 12 acres in Gurugram, delivered around 2025. One of the year’s largest transactions followed when Google leased about 617,000 sq ft there. The developer strategy is textbook institutional real estate: partner with global capital/operating expertise, develop an architecturally differentiated product, and secure anchor commitments from multinational occupiers before or around delivery. DLF’s broader commercial guidance is also revealing. Market commentary around DLF’s 2025 plans indicates annual commercial capex of roughly ₹5,000–6,000 crore and targeted yields on cost in the 18–25% range on incremental projects. That says something important about Gurugram: the best developers still see meaningful economics in premium office development when location, product, and tenant quality are right. The lease structure here is pre-commitment-driven and typically long-tenure, because that is what modern corporate tenants want in a high-specification campus.

Navi Mumbai case study — Mindspace Airoli and the suburban scale play. Airoli is one of the clearest examples of how the Mumbai region has evolved from a monocentric office geography into a multi-node market. Publicly reported transactions show Wipro leasing about 387,000 sq ft in Airoli for 10 years, while Dow Chemical took more than 256,000 sq ft on a similarly long-term basis. Mindspace REIT’s FY2025 operating disclosures show an average rent for area leased across the portfolio of about ₹81 psf/month, which is well below core Mumbai levels but still solid enough to support institutional returns. The developer strategy here is not to compete with BKC on prestige; it is to win on scale, connectivity, and cost efficiency, especially for technology, professional services, data, and support functions that want the Mumbai talent catchment without CBD economics. The lease structure is accordingly skewed to large blocks and long tenures, and the financial logic is compelling: lower land basis than the island city, rising suburban demand, and a growing set of large occupiers willing to commit for a decade or more.

Hyderabad case study — Mindspace Madhapur and redevelopment-led value creation. Hyderabad’s next-cycle opportunity is captured well by Mindspace REIT’s redevelopment pipeline. In its FY2025 investor presentation, the REIT disclosed that Building 1 at Mindspace Madhapur, with 1.5 million sq ft of leasable area, was 100% pre-leased to a GCC, with estimated completion in Q1 FY2027 and a balance construction cost of about ₹5,031 million. In the same cluster, the Experience Center redevelopment of about 1.6 million sq ft had a balance cost of roughly ₹7,085 million. The operational context is equally important: Mindspace reported that 78% of Q4 FY2025 committed leasing area was taken by GCCs, and average rent for FY2025 leasing across the portfolio was around ₹81 psf/month. I read this as one of the strongest proofs in the Indian market that redevelopment plus pre-lease plus GCC demand can create a powerful office-investment equation. It also reinforces a broader point: in India, the next tranche of high returning office stock may come as much from repositioned existing districts as from greenfield supply.

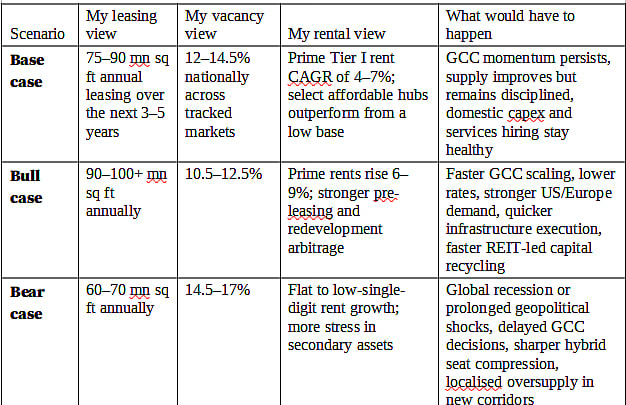

My base case for the next three to five years is constructive. The supporting evidence is strong: 2025 leasing reached 86.4 million sq ft, Q1 2026 annualised leasing already points to roughly the high-80s again, GCCs leased a record 31.3 million sq ft in 2025, ICRA expects 50–55 million sq ft of additional GCC demand in FY2026–FY2027, and Knight Frank argues India could add its next billion sq ft by 2036–2041 depending on the growth path. At the same time, supply is rising but not recklessly, and C&W explicitly notes that while completions should improve in coming quarters, quality availability remains tight enough that rents are expected to keep appreciating in prime submarkets. On that basis, my central expectation is for a market that remains landlord-friendly in premium corridors, tenant-selective in secondary stock, and increasingly bifurcated between institutional and non-institutional product.

These scenarios are my synthesis based on the 2025 leasing base, Q1 2026 run-rate, JLL’s GCC footprint outlook, ICRA’s GCC demand forecast, and Knight Frank’s stock-growth trajectory. They are not broker forecasts quoted verbatim; they are an analytical framework built from current market evidence.

The most immediate risks are not hard to identify. Cushman & Wakefield has already flagged Middle East-related geopolitical uncertainty and the potential for delayed deal closures. Academic evidence on remote work suggests continued risk to office valuations and construction in markets dominated by commodity stock. Knight Frank’s own rent and vacancy evidence also shows that where new supply spikes ahead of quality demand, vacancy can rise quickly even in otherwise healthy markets. In India, I would add one more risk that often gets underpriced: execution risk in emerging hubs. A city can announce a policy, a tech park, or a mega-campus, but if talent pipelines, transport access, and social infrastructure do not mature together, monetisation can lag for years. Surat’s experience is the clearest reminder.

For occupiers, my recommendation is to stop treating office decisions as a pure procurement exercise. In prime metros such as Bengaluru ORR, Gurugram CBD, core Hyderabad, South/West Chennai, and select Pune corridors, large users should be prepared to pre-commit or at least secure optioned space earlier in the cycle, because the best assets are increasingly absorbed ahead of completion. At the same time, I would actively build a hub-and-spoke portfolio: core leadership, client-facing, or high-collaboration functions in prime metros; supporting, hybrid, or distributed teams in cities such as Ahmedabad, Kochi, Thiruvananthapuram, Indore, and Visakhapatnam, where the cost base can be lower and employee catchments different. The point is not decentralisation for its own sake; it is resilience plus labour-market reach.

For developers, I would be highly selective on where and what to build. The best opportunities are in four buckets. The first is transit-rich premium campus supply in the strongest GCC corridors. The second is phased mixed-use tech districts in credible affordable hubs. The third is redevelopment/repositioning of older stock into ESG-compliant premium product, because Knight Frank’s retrofit evidence is compelling and REIT case studies now show the economics of pre-leased redevelopment. The fourth is managed-office and flexible-office enabling infrastructure, because hybrid work has structurally enlarged that demand base. What I would avoid is blind speculative supply in markets that do not yet have demonstrable anchor demand or city-level operating depth.

For investors, the opportunity set is broadening. Cushman & Wakefield’s capital-markets report says institutional real estate investment hit about USD 1.6 billion in Q1 2026, with office assets taking 64% of inflows and Delhi NCR, Chennai, and Bengaluru among the top destinations; JLL also notes a sharp rebound in India real estate investment in Q1 2026, with domestic institutions and REITs remaining important stabilisers. In that context, I would overweight three themes. First, income-yielding Grade A portfolios with strong GCC and multinational tenancy. Second, development-led yield creation where pre-lease visibility exists, especially in Bengaluru, Hyderabad, and Gurugram. Third, emerging-market optionality in Ahmedabad, Thiruvananthapuram, and Visakhapatnam, where the next valuation uplift may come from ecosystem maturation rather than from immediate rent compression. The common denominator should be the same in every case: quality, governance, and asset-management intensity.

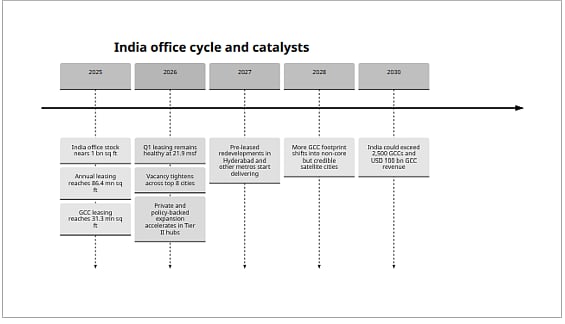

The timeline synthesises Knight Frank, JLL, C&W, and ICRA evidence and reflects the way I would sequence the next leg of India’s office cycle.

The biggest limitation in any pan-India office study today is the unevenness of data quality outside the top six cities. For Mumbai, Delhi NCR, Bengaluru, Chennai, Hyderabad, Pune, and increasingly Ahmedabad, there is enough broker coverage to speak confidently about stock, leasing, vacancy, and rents. For Indore, Jaipur, Kochi, Lucknow, Surat, and Visakhapatnam, the evidence is far better on specific parks, policy design, announced investments, and anchor occupiers than it is on citywide Grade A rents, vacancy, or average lease tenure. I have therefore chosen not to manufacture false precision where the market has not yet produced institutional-quality transparency.

A second limitation is that lease-term data are not published city by city-by-city in a standard form by most broker reports. Where I refer to lease cadence, I am using an informed market proxy based on public REIT disclosures, WALEs, and large registered leases rather than a formally published city average. That is analytically useful but not identical to a broker-maintained statistical series.

A third limitation is that policy regimes are moving quickly. GCC policies in Madhya Pradesh, Uttar Pradesh, Andhra Pradesh, and Maharashtra are recent and may be refined as states compete for mandates. In several emerging cities, commercial-market momentum could therefore move faster—or slower—than current evidence suggests, depending on execution. That is why I would treat this report as a strategy document anchored in the best currently available evidence, not as a substitute for micro-market diligence on a live transaction.

[Authored By Keval Valambhia- COO CREDAI-MCHI]