War has slipped its uniform and put on a trader’s suit. In the Gulf, the confrontation between Iran and the United States is no longer measured only in troop movements but in freight premiums, fuel bills and the pulse rate of financial markets.

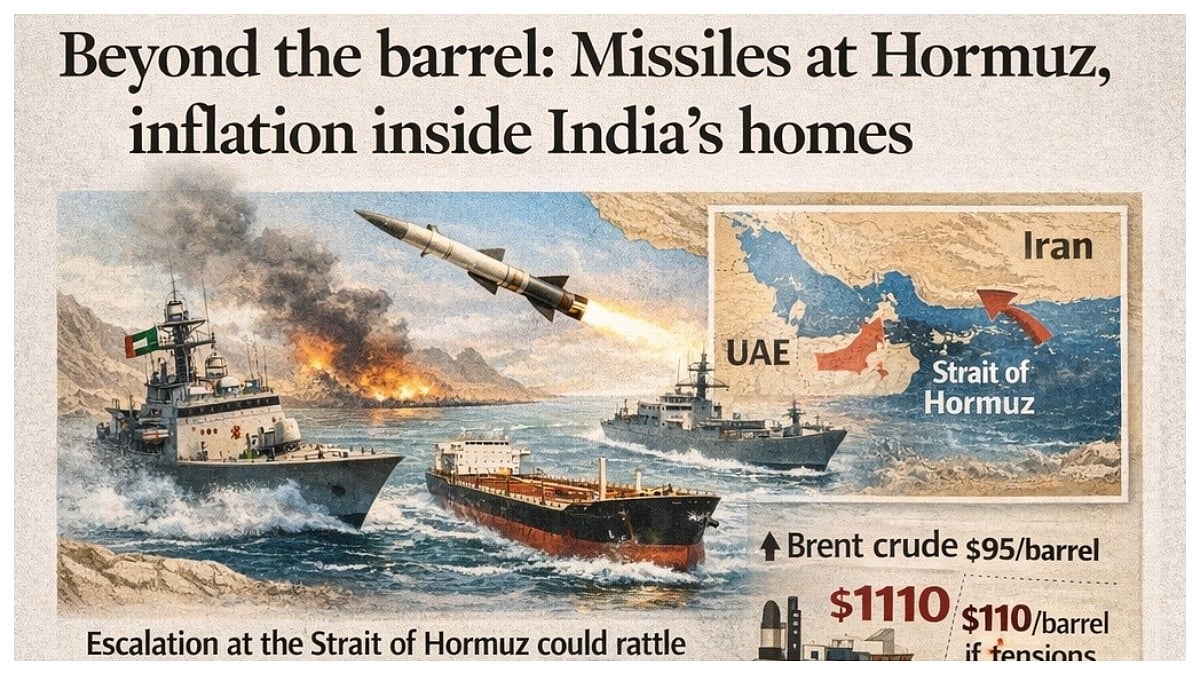

At the centre of this drama stands the Strait of Hormuz, a corridor so narrow that a single escalation can rattle the global economy. Tehran’s Revolutionary Guard proclaims control; Donald Trump signals naval escorts. Between these declarations, the world’s oil—and India’s inflation—holds its breath. Now Brent crude is on its way towards $95 a barrel. It is a reminder that geopolitics now trades in dollars as efficiently as in drones. Analysts warn crude could race towards $110 a barrel if the conflict widens or shipping is disrupted for weeks.

For India, the Gulf is not a distant theatre but a living artery. The six GCC states together account for over $180 billion in annual bilateral trade with India, spanning crude oil, gas, fertilisers, food and engineering goods. Nearly nine million Indian nationals work across Saudi Arabia, the UAE, Qatar, Kuwait, Oman and Bahrain, forming the largest expatriate community in the region. Their remittances—estimated at $60 to $65 billion a year—are not sentimental transfers; they are macroeconomic pillars, stabilising India’s balance of payments and sustaining millions of households from Malappuram to Muzaffarpur.

The nightmare scenario is brutally economic. A sustained disruption of Hormuz could remove a fifth of global oil supply from smooth circulation. For India, importing more than 85% of its crude, every $10 rise in prices drains foreign exchange, inflates transport costs and creeps into food inflation. The Reserve Bank and the Finance Ministry now track missiles with the same anxiety as monsoon clouds. Energy inflation would not merely dent growth; it would rewrite budgets and fracture consumption.

The GCC monarchies, too, face a perilous paradox. Higher oil prices swell treasuries, yet war threatens shipping insurance, aviation, tourism and the non-oil sectors painstakingly built over a decade. India’s exporters—rice traders, steelmakers and pharmaceutical firms—risk becoming collateral damage in a conflict they neither fuel nor fight.

Islamic revolutions have historically promised justice but delivered prolonged instability. Their aftershocks travel beyond borders, unsettling regimes and markets alike. In today’s Gulf, the fear is not only of drones and destroyers, but of political contagion that could test the durability of existing autocracies.

India’s diplomacy now resembles crisis management by spreadsheet. New supply routes, strategic petroleum reserves and discreet conversations with Washington, Tehran and Arab capitals form a policy of insulation rather than indifference. Yet insulation has limits when chokepoints close.

This war’s most dangerous theatre may not be the desert or the sea, but the invoice. If Hormuz tightens, inflation loosens. If tankers slow, remittances tremble. And in that ledger of risk, India emerges not as a combatant but as the most exposed spectator—a nation whose prosperity floats, quite literally, on a narrow strait patrolled by rival flags.