The recently published Report on Trend and Progress of Banking in India 2017-18 (https://www.rbi.org.in/Scripts/AnnualPublications.aspx?head=Trend%20and%20Progress%20of%20Banking%20in%20India) brought out by the Reserve Bank of India (RBI) is a veritable goldmine of information on banking and non-performing assets (NPAs) in India. Read between the lines, and you get a fair idea of what has gone wrong with banking in this country.

Take for instance the table given below.

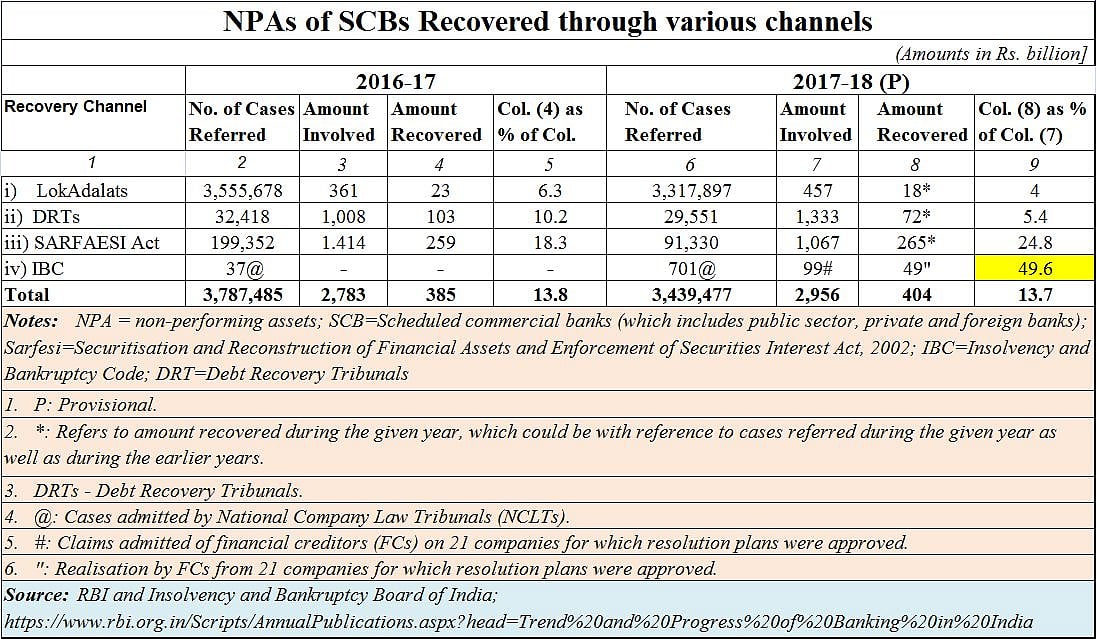

It will tell you of how different types of debt recoverysystems functioned in India. Watch the numbers in column 9. The figures inthese columns will tell you how efficient NPA resolutions systems have been. Itwill tell you that the least efficient was the Lok Adalat route to NPAresolution. Then, in the pecking order, came the debt recovery tribunals(DRTs), followed by proceedings under the SARFAESI Act, and finally the IBC orthe Insolvency and Bankruptcy Code.

IBC managed to recover almost Rs 49 billion of the Rs 99billion that was involved. That gives this method a recovery rate of 49.6%. Butthere are good reasons to hold the applause for a while. Study the numbers incolumn 6. They give you the number of casesthat were referred to each type of NPA resolution mechanism. Thus the LokAdalat was burdened with 3,317,897 cases during 2017-18. As many as 29,551cases were referred to the DRTs. SARFAESI accounted for 91,330 cases.Interestingly, only 71 cases were admitted by National Company Law Tribunals(NCLTs) under the IBC.

By focussing on fewer cases involving very large sums ofmoney, the NPA resolution system under the NCLT could cope more effectivelywith resolving the issue of bad debts than other mechanisms could. When you burden a system with too many casesand don’t even bother to increase the number of people who can deal with suchcases, you actually create a situation where justice will not be delivered, andthe malaise is allowed to fester. If more NCLTs (and more people) are not put intoplace as the number of cases mount, expect the IBC also to end up like the LokAdalat, DRT and SARFAESI.

Part of India’s problem of bad debts is the ever present hand of the politician-bureaucrat combine to grant loans to the undeserving, by breathing heavily down the necks of bankers. Then they ensure that the debt recovery mechanisms are burdened with too many cases. This is further compounded by allowing very few people to adjudicate matters, so that the pile-up of cases ensured little resolution. This has been done with the courts till now. Debt recovery mechanisms are neutralised using the same strategy (http://www.asiaconverge.com/2018/09/3-measures-can-stop-india-becoming-failed-state/)

All along India has specialised in creating systems designedto defraud, then structured to ensure that the guilty do not get penalised(http://www.asiaconverge.com/2018/08/banker-scams-ter-and-visible-hand-make-merry/).

That could explain the terrible state of public sector banks(PSBs) compared to private and foreign banks. The RBI reports tells you how, in2017-18, public sector banks accounted for NPAs worth almost Rs 9 lakh crore.In sharp contrast, private banks accounted for just 1.3 trillion of NPAs whileforeign banks accounted for barely Rs 138 billion. The buck stops at thedoorstep of the largest shareholder of the worst performers (the PSBs) whichhappens to be the government. It just did not (want to) set things right.

As a result, in 2017-18, you have PSBs accounting for 14.6%of gross NPAs, while private banks registered 4.7% and foreign banks 3.8%.Collectively, all scheduled commercial banks accounted for gross NPAs of 11.2%.

Current capital adequacy norms require banks to have atleast one-tenth of their advances as owned funds (share capital plus reserves).With gross NPAs hovering at 11.2%, it is quite clear that the banking sectorhas eroded its own capital. And with the government proposal in Parliament forenhancing bank recapitalisation outlay from Rs 65,000 crore to Rs 1,06,000crore, it is obvious that the Indian banking sector will continue to limp.

Add to this the flight of investment funds away from India,the worsening borrowing climate thanks to the clamour for loan writeoffs, andthe global economic slowdown that is likely to maul all countries in the world,expect the banking sector to continue hobbling along during 2018-19.

The government’s unwillingness to ask the electioncommission to ban the announcement of loan waivers is worrisome. It means thatthe door for offering loan waivers has been kept open. That does not augur well— either for the farmers whose loans are sought to be written off, or even thebanking sector.

The pains in the financial sector are far from over.

RN Bhaskar is consulting editor with FPJ.