The year 2016 has been quite happening for power sector with soft coal prices; visibility of regular supplies; mitigation of financial stress on balance sheets; and power trading getting to critical mass level. But on ground, there is still lot of work left to be done, both in terms of curtailing the transmission and distribution (T&D) losses ratio as well as doing justice to the investment done in the past decade, analyses PANKAJ JOSHI.

There are huge targets set by the government in terms of electrifying the country but the process involved in electrifying, is not as easy as it sounds. In India, power generation and distribution has always been a complex business, all the more for thermal power, where economics of the activity takes a back seat and other socio-political factors come into prominence. Also, marginalising of the economy is impacting a stunting capacity growth of the sector and is a bad sign for a power deficit economy. It is also reflected in sundry other areas like coal block allocation scams; power projects sanctioned without power purchase agreements; and weak balance sheets of state-owned power distribution companies (Discoms). These discoms also play an important role in banking sector’s NPA crisis.

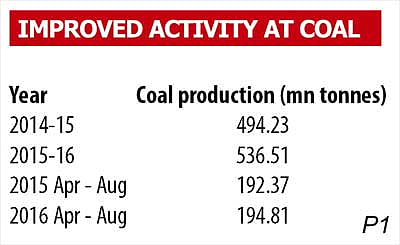

Coal availability was a major complaint point when a lot of large power projects were sanctioned. But one of the upfront positives for the sector is coal procurement issues which had dogged it badly in the first half of this decade and have been progressively mitigated. Coal prices worldwide have softened, in line with other fossil fuels, and supply outlook now is robust to the point of an oversupply situation. Coal India’s supply of coal for power generation went up from 385 million tonnes in 2014-15 to around 409 million tonnes in 2015-16. Secondly, Coal India has also got its act together.

The data (table P1) indicates the growth in its output and despatches in FY2016, which show a growth of around 8.5 per cent. Coal India crossed the half-billion tonnage mark for the first time, and the declared target for 2020 as one billion tonnes. Currently, Coal India accounts for 80 per cent of the total domestic coal production. Out of the 65 billion tonnes of Indian coal reserves, a techno-economic feasibility studies has only been done on mines with reserves around 30 billion tonnes. This could support the domestic thermal power capacity and make it relevant for a substantially long period for all stakeholders – employees, vendors, lenders and investors.

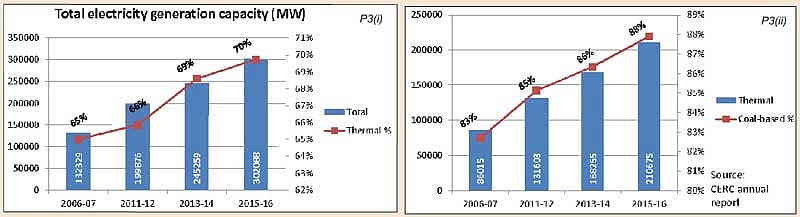

The importance of thermal power and of coal in thermal can be understood through table P3 (i) and P3 (ii). The overburden removal activity of Coal India also registered a 29.60 per cent growth in FY2016 which lead to facilitation of higher mining activity in future, which will increase production and despatches sustainable.

In terms of targets, the despatches in the April-August period are only 88 per cent of the target, vis-à-vis the corresponding 96 per cent in the same period last year. One can attribute the large slippage of coal offtake scenario to strikes and severe monsoon. This is a direct reflection of the growth in manufacturing and power generation which is still tepid. In Maharashtra, four plants of the state-owned Mahagenco (Koradi, Khaparkheda, Bhusawal and Parli) have been shut down due to insufficient demand from the local Discom and the Regulatory Commission’s diktat – if cheap power is available for purchase then it must be sourced before costlier (own generated) power. This throws light on the high-cost operations of the generation company compared to private players, as well as a reflection on how renewable power is slowly getting a footprint together in the state. Similarly, all three thermal power generation plants of the Punjab State Power Corporation Limited have shut down recently. Power sector contributes around 75 per cent to the coal offtake and growth in FY2016 was 6 per cent, which is lower than the overall despatches growth. The online route taken for coal purchases and the coal block auctions is a testimony not only to administrative skill but also political will. The block ownership transfer process continues to have some trouble. Likewise, the sluggish demand scenario is reflected in the pace of development of blocks where transfer is completed. In the previous phase (up to 2011-12), coal prices were strong and a scarcity premium factored into those prices, which incentivised the process of coal block development for production. The same is now absent and no change seen in the foreseeable future. Hence, even as the process is free of slurs of corruption, the economic recalculation of the same is yet to be reflected.

The Government came up with the Ujwal Discom Assurance Yojana (UDAY) to improve their financial structure, along with addressing the core issues of metering and collection which had led to their financial losses.

The UDAY blueprint is very clear in its approach – sustenance for losses is finite and a lot of cash generation should come out of own performance.

UDAY’s impact is visible in rural reach enhancement and urban efficiency. With limited centre exposure and strict result-based bank financing, there is a total move away from the blanket subsidy or loss-bearing attitude of the past. On the Discom front, there is some quantifiable action. The balance sheets have seen some relief as bad loans were taken over and converted into bonds. This resulted into reforming the needs in the T&D space. The consumer mapping initiative has been finished off before its scheduled timeline of March 2017. Mapping helps to get a grip on both the metering gap and the collection deficiencies. All these are very positive steps. The capex requirement estimates for the T&D space are also in place, but the grey area here is implementation of timelines. The T&D improvements basically are state-dependent and in all this, the local authorities are indeed being pushed for improvements in the T&D infrastructure and to deliver better power. Many states have indeed signed MOUs for augmentation of the same and ordering of equipment has also commenced. There is a lack of periodical update of implementation scoreboard. As of now, there is no scope of an update till the closure of the financial year, which can result to slippages. A quarterly/ half-yearly reporting system is needed.

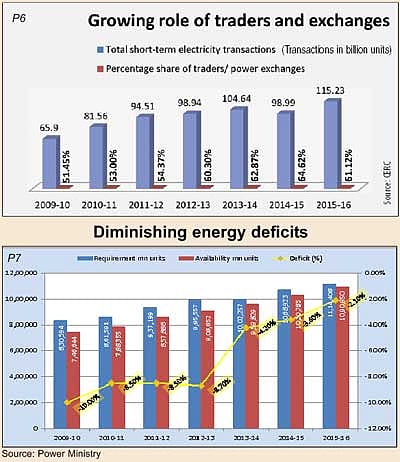

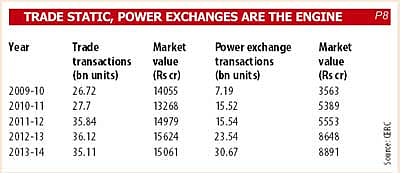

Another important development, gradually and without fanfare, is the improved volume trade on the power exchanges. Under the CERC guidelines, electricity trading currently happens through trading licencees and through two exchanges, the Indian Energy Exchange and the Power Exchange of India Limited. Like all marketplaces, the purpose of these exchanges is to create a trading environment which is more transparent, efficient and competitive. This purpose has been facilitated by multi-buyer and seller environment, real-time access to different volumes and prices for each seller state, along with equal access to the back-end transmission and distribution infrastructure. Several western countries have well-developed electricity trading markets where trade happens not only internally but, as in the European market, even across borders. For example, an IBEF report refers to the Nord pool as the combined power market. For India, the imperatives of having a power trading mechanism are obvious. Firstly, there are regional imbalances where states which create facilities for industries often find their power generation insufficient. Agriculture sees such anomalies – a good monsoon causes production issues, while the demand simultaneously goes up for the particular cropping season, and spills over into other sectors in the latter part of the fiscal year. The CERC estimates that the total volume of short-term transactions of electricity increased from 65.90 billion units (BU) in 2009-10 to 115.23 BU in 2015-16. When the earlier years were witnessing unnaturally high average unit transaction prices (speculation-driven), the CERC had stepped in and put in a ceiling which had a cooling-off effect. The fact that higher volumes are being generated today at these prevailing lower average transaction prices (P2 and P8), are a reflection of the day-to-day market economics. A high range of volatility is not unusual across the globe – data available for the Nord pool for 2012 displays a price range of € 12.46/MWh to € 54.10/MWh.

Right now, the exchanges have:

The share of traders and power exchanges in total short-term electricity transactions went up from 51 per cent in 2009-10 to 61 per cent in 2015-16 (P6). This was due to power exchanges. Additionally, there was a dormant short-term market for power which is being reliably tapped through the power exchanges now. The exchanges are characterised by increase in volume traded, increase in liquidity and reduced price volatility over time.

[alert type=”e.g. warning, danger, success, info” title=””]

Sector in a jiffy

In policy front, the sector is already moving ahead. There is well-thought out policy action and bureaucratic hurdles are now getting easier to negotiate.

Input (coal) prices are soft and set to remain so.

Upcoming investments in T&D infrastructure will complement generation, and ensure more penetration into non-industrial consumers, as well as proper monitoring and billing.

The political/ bureaucratic action needs a monitoring mechanism which is more robust and more frequent, plus has a greater degree of accountability.

The less controllable, factor is the current state of the economy. Demand from the industry segment, the largest and most profitable client segment, stands out as a major concern for the power sector.

[/alert]

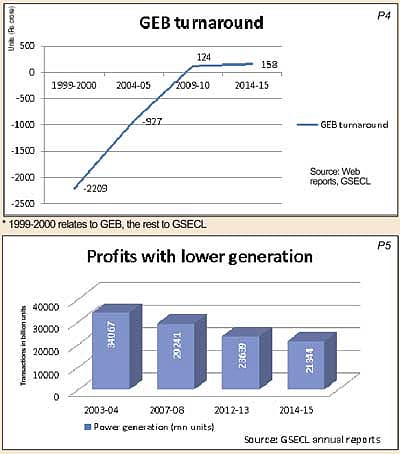

Regarding the timeline for the improvement in financial status, it is pertinent to note the case study of the Gujarat Electricity Board (GEB) (P4). Gujarat has always been among the premier states as far as business and industries are concerned. Yet the GEB ran into huge losses for almost seven years, starting from the mid-nineties. While the manufacturing slowdown was one of the factors for the transmission losses, the other internal factors that were at work were lack of efficiency in generation operations, metering and monitoring issues in T&D; and a tithe of political interference. The diagnosis rings somewhat true even today for the sector, but what followed was a restructuring exercise in 2001 on the initiative of the state government.While the standard tactics of unbundling the three activities into different companies were followed, what was a more novel approach was curbing the theft-and-unbilled losses in the T&D segment, called the Jyotigram Yojana. The idea was to use a separate feeder network for domestic use (with specially designed transformers), and provide limited supply in non-peak hours to agricultural users. The state government invested Rs 1,200 crore, and obtained manifold benefits. Industries got quality power; village residential settlements were assured of standard and regular supply; and agricultural users got a pre-announced window, by which they could schedule their irrigation and any other uses. Regular and limited usage enabled them to save on water, labour and pump upkeep costs. The separation-cum-dedication mechanism got good implementation reviews and the impact can be seen in the results. T&D losses dropped from 35 per cent in 2003 to 19 per cent in 2012. From a loss of Rs 2,209 crore in 1999-2000 (erstwhile GEB), the GSECL made a profit of Rs 200 crore in 2005-06 and it has been profitable consistently since then. The fact that these profits are achieved on lower generation (P5) volumes itself is testimony to both improved work efficiencies as well as lower T&D losses. In a report by the Stockholm International Water Institute on the Jyotigram Yojana, “Rural Gujarat has been completely rewired. Villages are given 24-hour, three-phase power supply for domestic uses, in schools, hospitals, and village industries, all at metered rates. The separation of agricultural energy from other uses and the promise of quality supply were sufficient to gain political and social backing for implementation.” However, the implementation took time but it did yield results.