Want To Change Your Tax Regime While Filing ITR? Here's Who Can Switch & Who Gets Only One Chance?

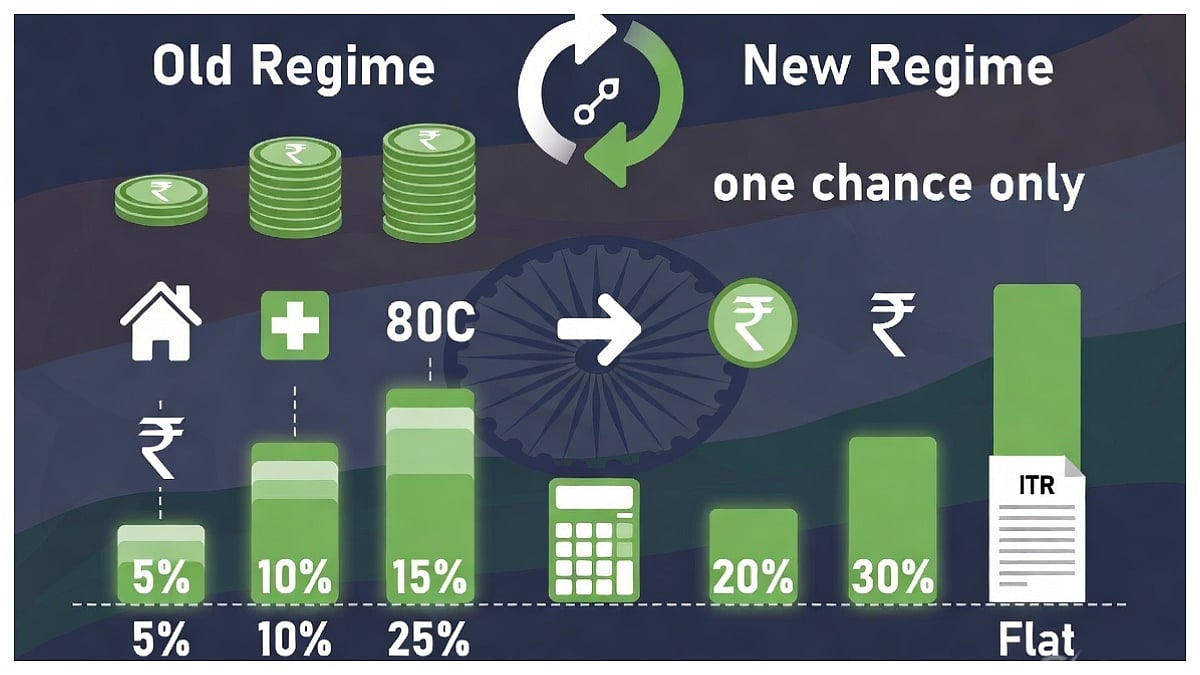

Taxpayers can change their tax regime while filing their income tax return, but the rules differ for salaried employees and those with business or professional income. Salaried individuals can switch every year, while business taxpayers get only one lifetime opportunity to move back to the old regime.

Mumbai: Many taxpayers believe they are stuck with the tax regime selected by their employer. However, that is not always true. The Income Tax Department allows eligible taxpayers to change their tax regime while filing their Income Tax Return (ITR), subject to certain conditions.

The rules are different for salaried employees and those earning business or professional income.

Who Can Switch?

Salaried individuals enjoy greater flexibility. Even if an employer has selected the new tax regime as the default for salary deduction during the financial year, employees can still choose the old tax regime while filing their ITR.

This option is available every assessment year. As a result, salaried taxpayers can compare their tax liability under both regimes before making the final choice at the time of filing their return.

However, the rules are stricter for taxpayers who earn income from a business or profession.

Individuals filing ITR-3, ITR-4 or ITR-5 can shift from the new tax regime to the old tax regime only once in their lifetime. To exercise this option, they must submit Form 10-IEA before filing their return.

How To File Form 10-IEA

Taxpayers can file Form 10-IEA through the Income Tax Department's e-filing portal.

After logging in with their PAN and password, they need to visit the Income Tax Forms section, select Form 10-IEA, choose the relevant assessment year, and complete the required declarations.

The form asks taxpayers to confirm that they have business or professional income and that they wish to opt out of the new tax regime. After verifying all details, the form must be submitted online.

ALSO READ

Choosing The Right Regime

The old and new tax regimes have different tax rates and benefits.

The old regime allows several deductions and exemptions, while the new regime offers lower tax rates but permits only limited deductions.

The better option depends on an individual's income, investments and eligible deductions. Tax experts advise taxpayers to compare their tax liability under both regimes before making the final decision.

The Income Tax Department's online Income and Tax Calculator can also help taxpayers estimate the tax payable under each regime before filing their ITR.

RECENT STORIES

-

-

-

-

-